Update from CIG Asset Management: Extremes May Create Opportunities

The stock market rally continues. Through June 13, 2024, the S&P 500 has gained +14.7% year-to-date and we still haven’t seen a single-day decline of over 2% in 479 days, the third longest stretch in the past 25 years. [i] We wrote about this extraordinary winning streak in last month’s update, Where are we now?

This year, some investors who have a diversified portfolio that owns many stocks across many sectors, may feel like they are missing out on the current rally. They may see on CNBC or read in the Wall Street Journal that the market is at its all-time high, yet their own portfolio is not.

Closely examining the following extreme market internals; narrow sector performance, large market cap outperformance and S&P 500 index concentration can help explain what is happening beneath the surface.

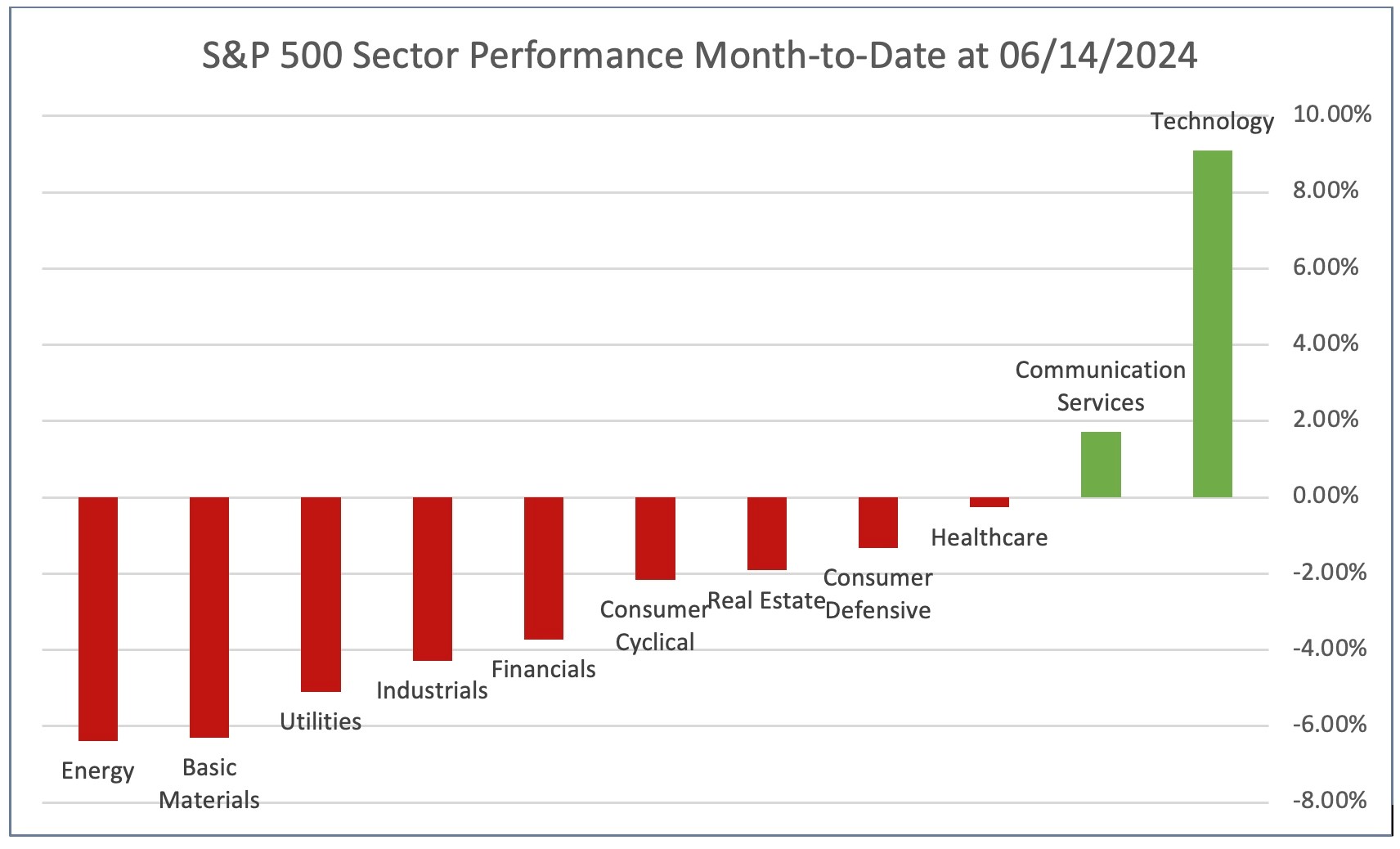

Sector performance is narrowing again. In our CIG Asset Management Update on April 1, 2024, we discussed encouraging signs that the stock market rally may be broadening. We may have been early on that call. As you can see in the chart below, month-to-date at June 14, 2024, the technology sector has gained +9.1%, communication services – which is mostly comprised of Meta and Google – advanced +1.7%, and the other nine of the eleven S&P 500 sectors were all down. [ii]

Chart by CIG Asset Management using data from FinViz

Chart by CIG Asset Management using data from FinViz

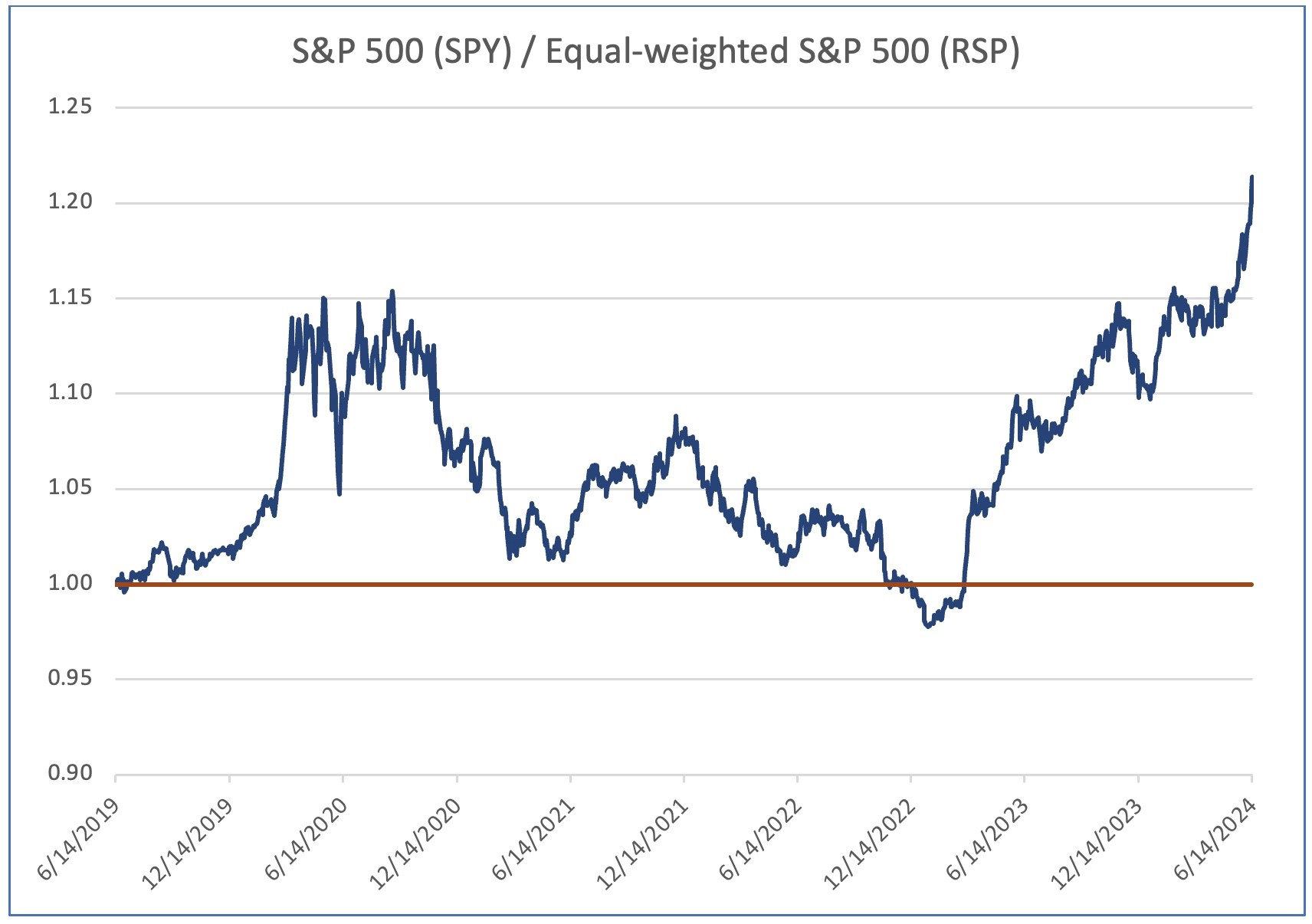

Large market-cap out performance. The S&P 500 index is weighted by market capitalization– that is, the larger the total value of the company, the higher the weighting in the index. It’s currently experiencing historic outperformance versus the equal-weighted S&P 500. In fact, while the S&P 500 – represented by the SPDR S&P 500 ETF Trust (SPY) has advanced +14.6% year-to date through 06/14/2024, the equal-weighted S&P 500 500 – represented by the Invesco S&P 500 Equal Weight ETF (RSP) is only up +4.2%. [iii] .

The following chart shows the relative performance of the market-cap weighted S&P 500 (SPY) versus the equal-weighted S&P 500 (RSP) for the 5-year period ending June 14, 2024. When the blue line is below 1.0, RSP is outperforming SPY. As you can clearly see, this has been a rarity over the past five years.

Chart by CIG Asset Management using data from Barchart.com.

Chart by CIG Asset Management using data from Barchart.com.

The slope of the blue line has recently been increasing – this indicates that the outperformance is widening. This tells us that the larger companies are outperforming the smaller companies. What companies are outperforming? The answer is large-cap stocks in the technology sector, and we believe their returns are being driven by the hopes that Artificial Intelligence (AI) will contribute massive revenues and earnings to this sector.

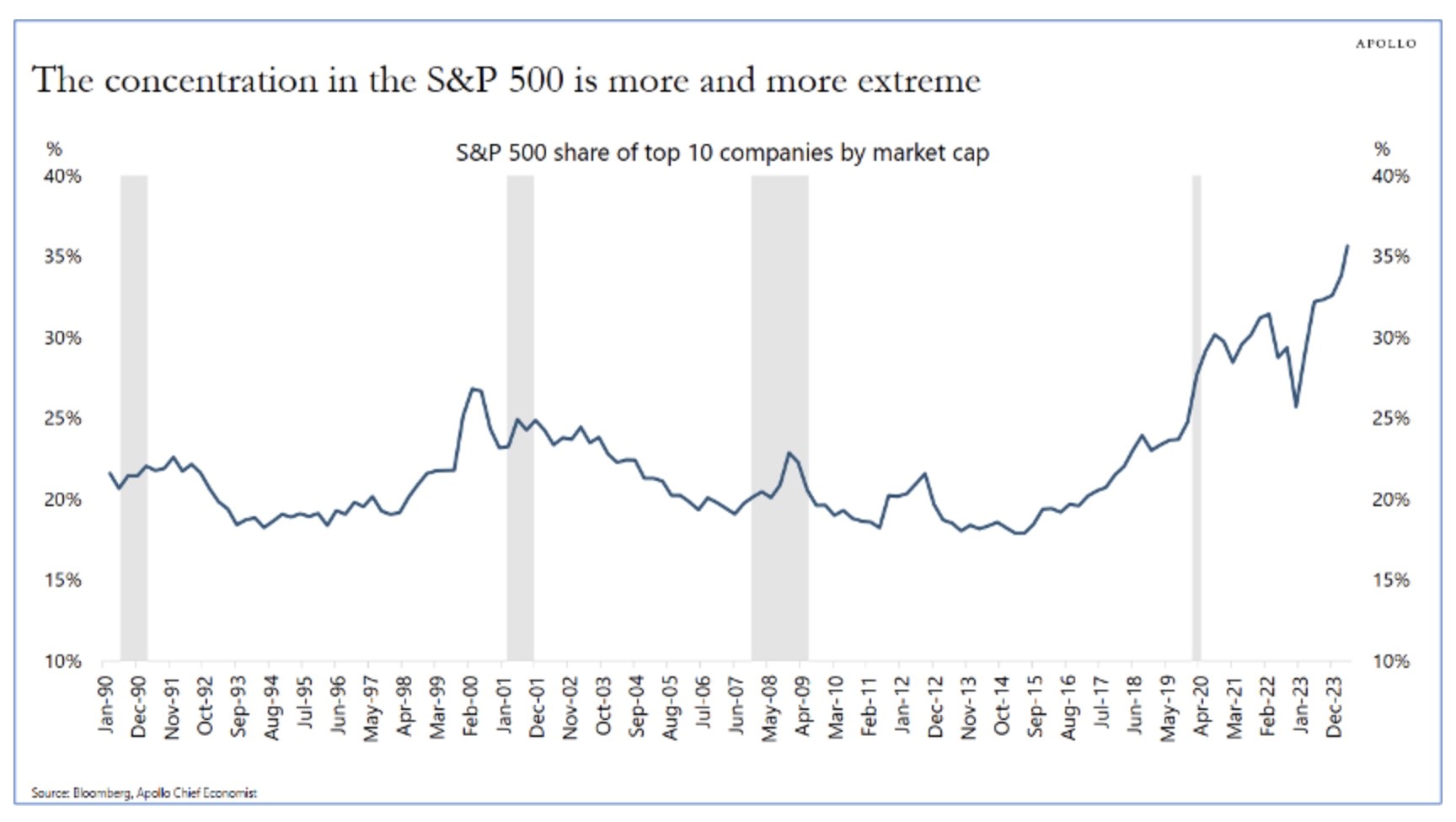

S&P 500 index concentration. On June 9, 2024, Apollo Chief Economist Torsten Slok posted the following chart in The Daily Spark.

Source: Apollo The Daily Spark 06/09/2024

Source: Apollo The Daily Spark 06/09/2024

Currently, ten out of the 500 stocks in the S&P 500 account for over a third of its total value. These high-growth stocks have been major contributors to recent S&P 500 returns. Such extreme concentration is rare. Only three of those ten largest companies are outside of the Technology or Communications sectors: Berkshire Hathaway, Eli Lilly and JP Morgan. [iv] This is great when the top ten are moving higher and add excess returns to the market cap weighted S&P 500 index but can have the opposite effect if the hopes that AI will produce enormous profits for the companies involved does not prove to be true.

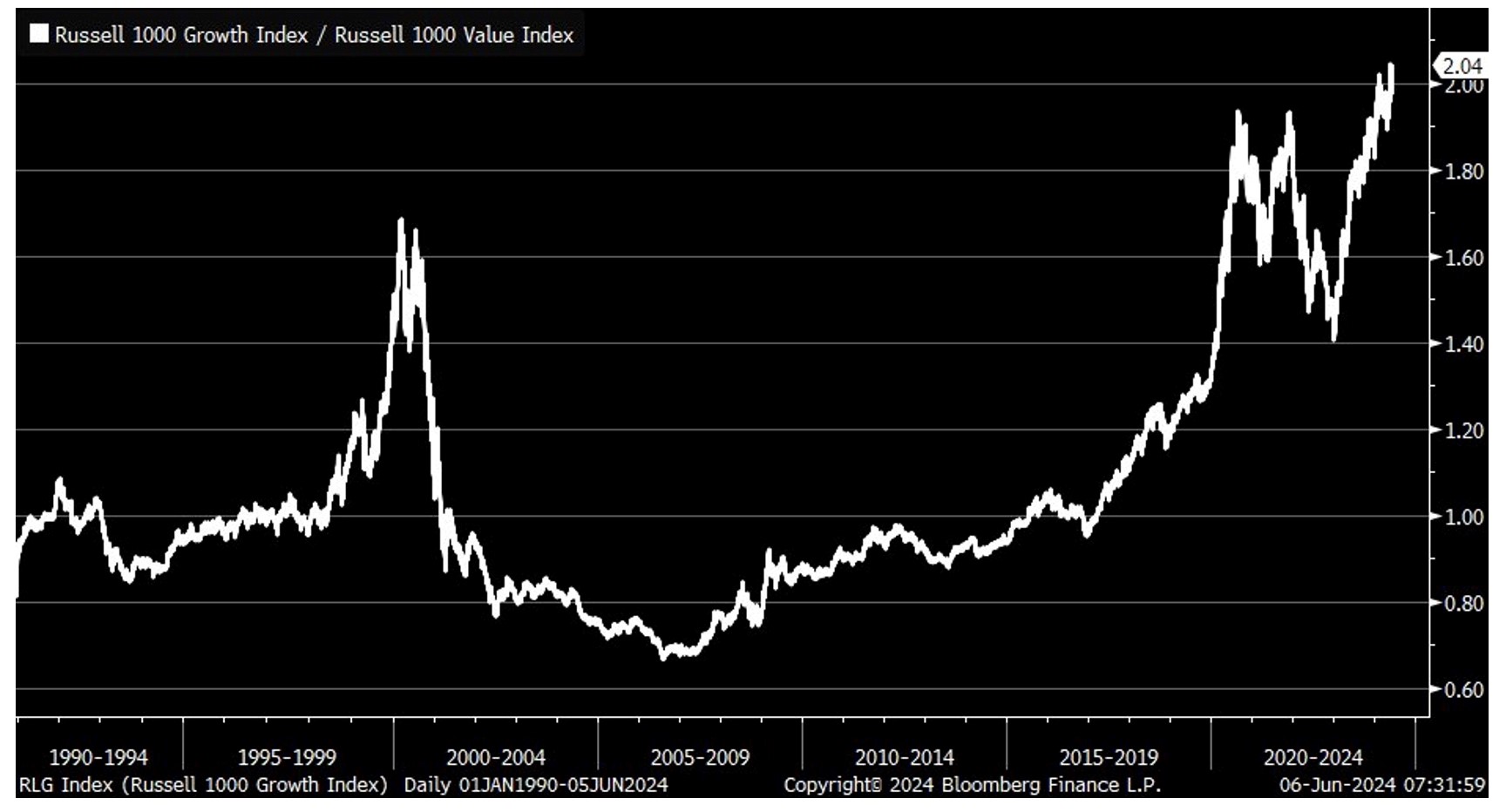

Growth versus Value. The following chart shows the ratio of the indexed returns of the Russell 1000 Growth Index and the Russell 1000 Value Index. The Russell 1000 Growth Index is currently outperforming the Russell 1000 Value Index by the biggest margin in decades! As of June 14, 2024, nine of the top ten stocks in the iShares Russell 1000 Growth ETF – which tracks the index – were technology related stocks and were a total of 53%, of the index. [v]

Source: Bloomberg 06/06/2024

Source: Bloomberg 06/06/2024

1. Value may once again outperform growth. The significant spike in the year 2000 during the dot-com bubble serves as a historical reference. Right now, we’re witnessing another surge in large-cap technology stocks, which we attribute to an AI bubble. In 2000, after the dot-com bubble burst, value stocks outperformed growth stocks. We’ve strategically positioned our clients’ portfolios to potentially benefit from this trend if the AI bubble deflates.

2 Profit-Taking and Rebalancing: When a sector or set of stocks significantly outperforms, we consider taking profits and rebalancing client portfolios. This can be an attractive exit point. We will look for tax harvesting opportunities as well as we rebalance.

3. Buying Opportunities: Conversely, when a sector or set of stocks underperforms, it may present an opportune entry point. To take advantage of this opportunity, we look to add positions before a sector recovers.

4. Contrarian Approach: Small-cap stocks and value stocks, often overlooked during market extremes, might be particularly appealing to contrarian investors right now. Year-to-date through [June 14, 2024], the Russell 2000 index of small-cap stocks is down -1.0%. [vi]

In navigating these market dynamics, we recognize that extremes can create opportunities. Whether it’s profit-taking, rebalancing, or adopting a contrarian approach, staying informed and maintaining an active management strategy will be crucial. In doing so, we continue to manage diversified strategies for the long run.

Please reach out to Brian Lasher (blasher@cigcapitaladvisors.com), Eric T. Pratt (epratt@cigcapitaladvisors.com) or the rest of the CIG team.

[i] Calculated by CIG Asset Management using data from finance.yahoo.com

[ii] Calculated by CIG Asset Management using data from finance.yahoo.com

[iii] Calculated by CIG Asset Management using data from finance.yahoo.com

[iv] Calculated by CIG Asset Management using data from finance.yahoo.com

[v] https://www.ishares.com/us/products/239706/ishares-russell-1000-growth-etf

[vi] Calculated by CIG Asset Management using data from finance.yahoo.com

CIG Asset Management Update: Infrastructure, Gold, and Strategic Positioning in a Changing Landscape

In our October 2023 CIG Asset Management Update: Year-to-Date U.S. Stock Performance in Pictures, we discussed our theme of Clean Transition Investing as a possible alternative way to participate in the stock market without chasing the Magnificent 7 stocks. [i] This theme focuses on the 2015 Paris Agreement, which outlined the long-term goal of reaching net zero emissions by the year 2050. However, global spending fell short in 2023, reaching an estimated $1.8 trillion out of the necessary $5 trillion annually. [ii]

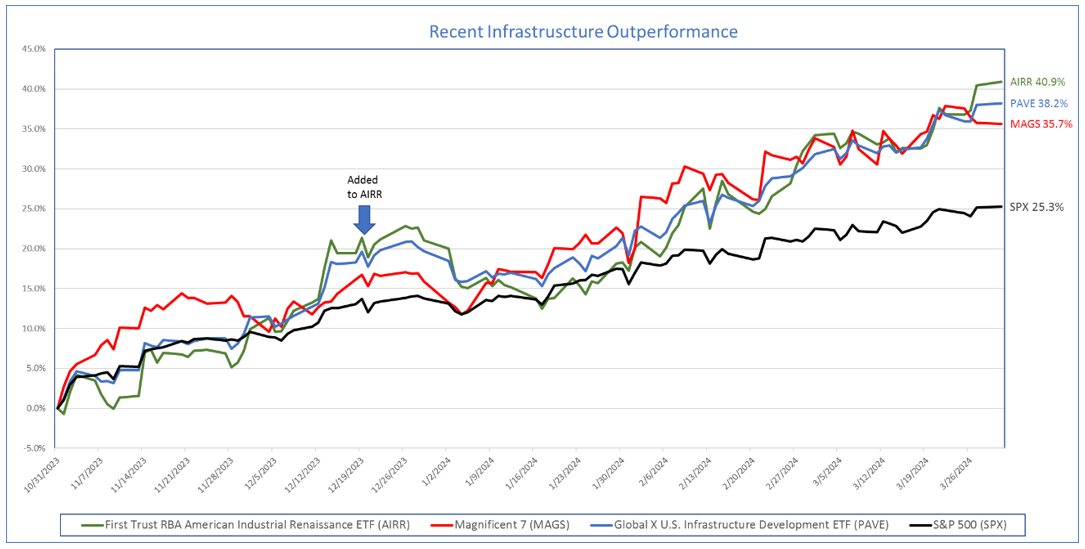

We initially bought First Trust RBA American Industrial Renaissance ETF (AIRR) to participate in Clean Transition Investing for our CIG Dynamic Growth Strategy and CIG Dynamic Balanced Strategy in September 2023. We then added more AIRR in December 2023. Most recently, we added an additional investment in the Global X U.S. Infrastructure Development ETF (PAVE). How are these investments doing?

As seen in the chart below these infrastructure investments, (AIRR) and (PAVE) outperformed the Magnificent 7 stocks (MAGS) and the S&P 500 (SPX) for the period October 31, 2023, through March 31, 2024.[iii]

Data from Barchart.com for the period 10/31/2023 to 3/31/2024

Past performance is not indicative of and not a guarantee of future results, but we are encouraged that it it may be possible to enjoy positive market outperformance without chasing the Magnificent 7 stocks which, in our opinion, are in a bubble.

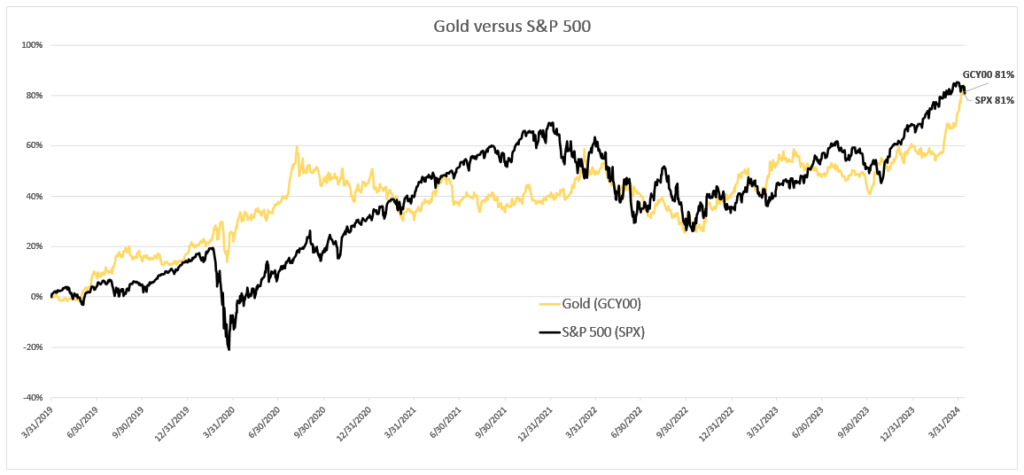

Moving on to another asset class, as of April 19, 2024, Gold futures closed at an all-time high of $2,398.40 / ounce on the COMEX exchange. [iv]As illustrated in the chart below, for the period March 31, 2019, to April 12, 2024 – just over five years – Gold, (symbol GCY00) has captured 100% of the S&P 500’s return! [v]

Data from Barchart.com for the period 3/31/2019 to 4/12/2024

Perhaps more impressively, from the peak of the dot-com boom in March 2000 through April 10, 2024, The S&P 500 has gained +244%, but Gold gained +738% – triple the return! [vi] Gold and miners continue to be a part of many of our client’s managed portfolios.

Why has Gold enjoyed such a stellar performance?

According to the latest budget update from the Congressional Budget Office (CBO), the U.S. government ran a staggering budget deficit of $1.7 trillion in fiscal year 2023. This deficit represents 6.3% of the country’s gross domestic product (GDP), significantly surpassing the 3.7% average observed over the past 50 years. Notably, excluding the Great Financial Crisis and the COVID-19 pandemic, this deficit-to-GDP ratio is the highest since World War II. [vii]

In 2023, the government’s net interest costs reached a staggering $659 billion, marking an 87% increase compared to the amount in 2021. [viii] The CBO’s latest projections also raise concerns: total U.S. federal government debt is projected to climb from 97% of GDP last year to 116% by 2034—surpassing the debt levels seen during World War II. Bloomberg Economics conducted extensive simulations to assess the fragility of the debt outlook. Alarmingly, in 88% of these simulations, the results indicate that the debt-to-GDP ratio is on an unsustainable trajectory, signifying an increase over the next decade.[ix] These unwieldly debt obligations and large budget deficits could potentially weaken the U.S. dollar relative to other currencies.

The weaponization of the U.S. dollar became evident following Russia’s invasion of Ukraine, leading to unprecedented financial repercussions for Putin’s regime. World leaders are now actively reducing their reliance on the U.S. dollar.[x]

On April 8, 2024, U.S. Treasury Secretary Janet Yellen issued a stern warning in Beijing: “Banks facilitating significant transactions related to Russia’s defense industry risk U.S. sanctions.”[xi] Russia’s Foreign Minister Sergey Lavrov met in Beijing to counter mounting pressure from the U.S. and its allies.[xii] Simultaneously, central banks worldwide are diversifying away from U.S. dollar reserves. They’ve been accumulating gold reserves at an astonishing pace—over a thousand tons in 2022 and 2023.[xiii] As other countries grow wary of holding U.S. assets due to potential reprisals, gold emerges as an increasingly attractive investment. The question remains: How will the United States manage its debt if global confidence in dollar-based assets wanes? Of note, as the dollar weakens, investments outside of the U.S. become more attractive to investors. At CIG, we are keenly focused on exploring international investment opportunities to capitalize on this trend.

America’s debt-to-GDP ratio is regaining the heights last seen post WWII. Past periods of sacrifice tended to be followed by burden-sharing and higher taxes. In 1932, as the Great Depression raged, America’s top marginal tax rate rose to 63% and continued higher through 1944 when it hit 94% on incomes over $200,000 (equivalent to $2.9mm in today’s dollars). The post-war economy boomed as America rebuilt the world. The top marginal rate remained above 90% until 1964 when we lowered it to 70%. [xiv] But today, we’re unsure whether we’ll make similar choices to raise taxes and share the burden. Nor do we know the societal consequences that come from refusing to equitably share our burdens.

In light of current conditions, our investment strategy remains nimble. We are encouraged by the recent performance of our new infrastructure investments. Equally noteworthy is our commitment to gold as a long-term asset, which has yielded productive results. The recent surge in gold prices, reaching an all-time high, underscores its resilience and attractiveness over the past five years-mirroring its performance since the Dot Com bust.

As we navigate the financial landscape, we maintain a cautious optimism, leveraging our insights and strategic positioning to potentially capitalize on opportunities while attempting to prudently manage risks. Our commitment to making prudent investment choices continues to drive results for out clients.

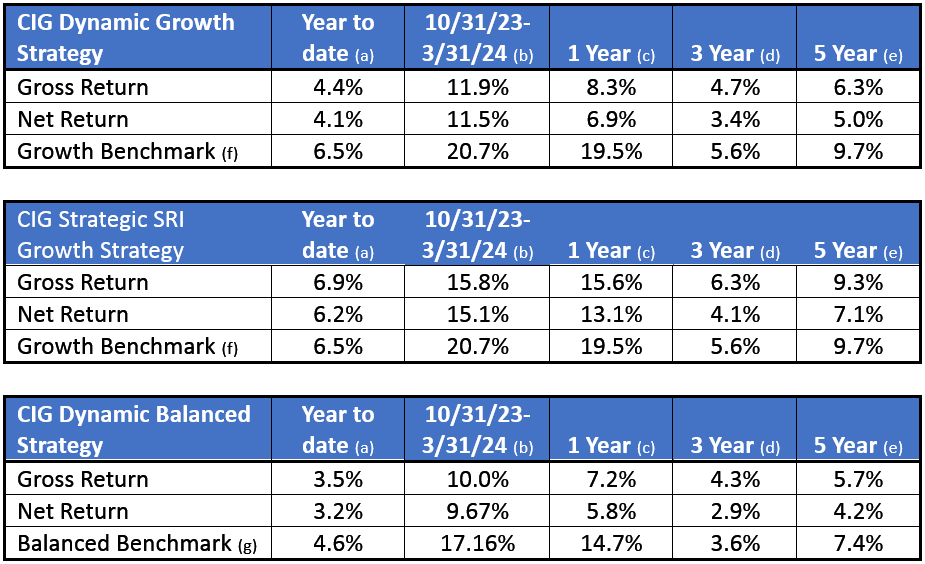

Strategy Returns as of 3/31/2024:

Performance has been attested to by ACA Group for the period August 1, 2018, through December 31, 2022.

Strategy returns are calculated independently on a daily basis and linked geometrically to produce a monthly return. Total investment performance includes realized and unrealized gains and losses, dividends, and interest. Accrual accounting is used to record interest income while dividends are recorded on a cash basis. Trade date accounting is used for calculation and valuation purposes.

Past performance is not indicative of future results.

(a) Represents performance from January 1, 2024, through March 31, 2024.

(b) Represents performance from October 31, 2023, through March 31, 2024.

(c) Represents performance from April 1, 2023, through March 31, 2024.

(d) Represents annualized performance from April 1, 2021, through March 31, 2024.

(e) Represents annualized performance from April 1, 2019, through March 31, 2024.

(f) The Growth Benchmark is a blend of 60% Russell 3000, 25% MSCI All-Country World ex US and 15% Bloomberg US Aggregate Bond indices.

(g) The Balanced Benchmark is a blend of 45% Russell 3000, 10% MSCI All-Country World ex US and 45% Bloomberg US Aggregate Bond indices.

[i] The ”Magnificent 7” stocks are Apple (AAPL), Microsoft (MSFT), Nvidia (NVDA), Alphabet (GOOG), Meta Platforms (META), Amazon (AMZN) and Tesla (TSLA). https://www.nasdaq.com/articles/the-easiest-way-to-remember-the-magnificent-7-stocks-and-why-you-should-care

[ii] GlobalX – Why Should You Consider Investing in U.S. Infrastructure Development?

[iii] Calculated by CIG Asset Management for using data from Barchart.com for the period 10/31/2023 to 3/31/2024

[iv] Data from finance.yahoo.com

[v] Calculated by CIG Asset Management for using data from Barchart.com for the period 3/31/2019 to 4/12/2024

[vi] Calculated by CIG Asset Management for using data from Barchart.com for the period 3/31/2000 to 4/12/2024

[vii] Data from https://www.cbo.gov/publication/60053 https://fred.stlouisfed.org/series/FYFSDFYGDP

[viii] Data from https://www.cbo.gov/publication/60053 https://fred.stlouisfed.org/series/FYFSDFYGDP

[ix] https://www.fastbull.com/news-detail/a-million-simulations-one-verdict-for-us-economy-3825714_0

[x] https://www.bloomberg.com/news/articles/2023-06-02/putin-s-war-ignites-backlash-against-dollar-across-the-world

[xi] https://www.bloomberg.com/news/articles/2024-04-08/yellen-threatens-sanctions-for-china-banks-that-aid-russia-s-war

[xii] https://www.nytimes.com/2024/04/09/world/asia/xi-lavrov-russia-china.html

[xiii] The High-Tech Strategist April 2, 2024

[xiv] Data from https://taxfoundation.org/data/all/federal/historical-income-tax-rates-brackets/

CIG Asset Management Update: The Stock Market Rally May Be Broadening

In October 2023, we shared the CIG Asset Management Update: Year-to-Date U.S. Stock Performance in Pictures and we discussed how the Magnificent 7[i], seven mega-cap growth stocks, were driving the returns of the S&P 500.

This outperformance continued through year end as you can see in the December 31, 2023 FinViz heat map below.

Source: FinViz as of 12/31/2023

In the year, 2023, the Magnificent 7 stocks experienced an average return of +111% while the S&P 500 Index only gained +26%. The Equal-Weighted S&P 500 Index only gained +12%. If you removed the Magnificent 7 stocks from the Equal-Weighted S&P 500 Index, you would have only gained +8%. [ii]

The strong performance of the Magnificent 7 stocks has extended into 2024. As of February 29, 2024, these seven stocks have gained +12.7%, outpacing the S&P 500’s increase of +7.1% and the Equal-Weighted S&P 500 Index’s gain of +3.2%.[iii]

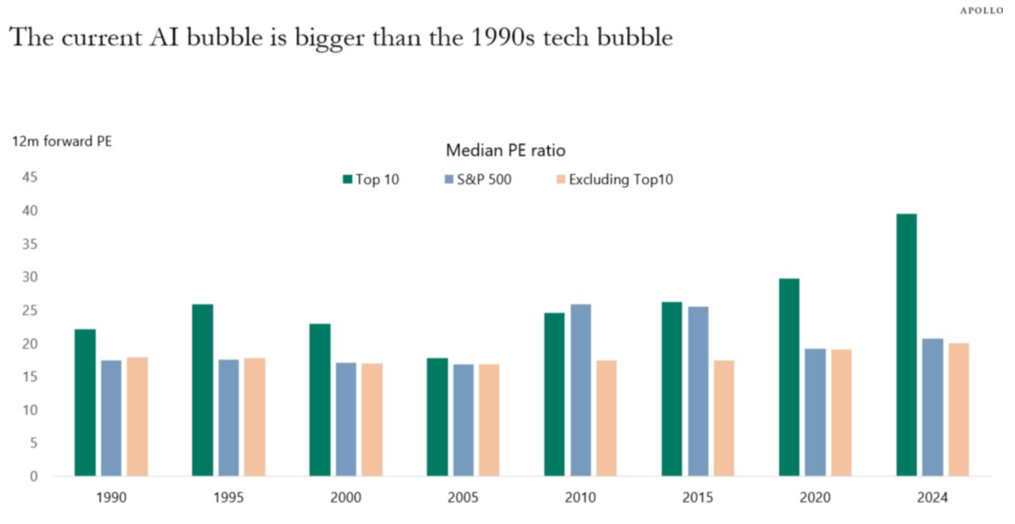

We believe the Magnificent 7 stocks are currently trading at levels considered expensive compared to historical standards. Torsten Slok, Apollo’s Chief Economist, has recently showed that when you compare the median 12-month forward price-to-earnings (PE) ratio of the top ten companies in the S&P 500, which include all of the Magnificent 7 stocks, they are much more expensive now than they were during the tech bubble of the 1990s. [iv]

Source:Bloomberg, Apollo Chief Economist. Note: Data as of January 31, 2024.

With that being said, we are seeing some encouraging signs that the stock market rally may finally be starting to broaden out. For the week ended 3/6/2024, we saw four of the Magnificent 7 stocks; Microsoft (MSFT), Apple (AAPL), Alphabet (GOOG), and Tesla (TSLA) move lower as many other stocks outside of the technology sector rose. You can see this in the March 6, 2024 FinViz heat-map below.

Source: FinViz as of 3/6/2024

While we find it encouraging to see a wider equity market participation, we still believe strongly in the value of diversification. Diversification is not supposed to maximize returns, it is designed to reduce investment risk. A diversified portfolio at times won’t keep up with the market when the bulk of returns are concentrated in a small group of stocks like the Magnificent 7. We strive to diversify our investments amongst industries and sectors, size (large-cap and small-cap), geography, growth versus value and alternative asset classes. Some of these investments are negatively correlated to the stock market – what that means is historically when the stock market traded lower – these investments gained in value. Past performance is not a guarantee of future results, but history helps guide us.

At CIG, we believe in risk-balanced investing. We believe investors should consider how much risk they are taking to achieve returns. We think that we should be striving to reach the return necessary to meet the various needs of our client’s financial plans while, at this point in the market cycle, taking as little risk as possible to meet that goal. We want you to sleep at night.

Please reach out to Brian Lasher (blasher@cigcapitaladvisors.com), Eric T. Pratt (epratt@cigcapitaladvisors.com) or the rest of the CIG team.

This report was prepared by CIG Asset Management and reflects the current opinion of the authors. It is based upon sources and data believed to be accurate and reliable. Opinions and forward-looking statements expressed are subject to change without notice. This information does not constitute a solicitation or an offer to buy or sell any security.

[i] The Magnificent 7 stocks are: Apple (AAPL), Microsoft (MSFT), Alphabet (GOOGL), Amazon.com (AMZN), Nvidia (NVDA), Tesla (TSLA), and Meta Platforms (META)

[ii] https://www.forbes.com/sites/greatspeculations/2024/01/22/2023-in-review/?sh=78aab8bd690b

[iii] Calculated by CIG Asset Management for the Roundhill Magnificent Seven ETF (MAGS) using data from finance.yahoo.com

[iv] The Daily Spark, February 25, 2024 – Apollo Academy

CIG Asset Management Update: A New Bull Market?

Summary:

* Are we in a new bull market?

* S&P 500 performance continues to be concentrated in only a few names.

June 2023 Returns:

| Benchmark / Index | Return | Benchmark / Index | Return |

|---|---|---|---|

| Growth Benchmark[i] |

4.7% |

Balanced Benchmark[ii] |

3.4% |

| S&P 500[iii] |

+6.6% |

Bloomberg US Agg Bond[iv] |

(0.4%) |

| MSCI EAFE[v] |

4.6% |

MSCI Emerging Markets[vi] |

3.8% |

| Gold[vii] |

(2.2%) |

Crude Oil[viii] |

+3.8% |

Commentary:

Domestic equities continued to rally in June after President Biden signed the Fiscal Responsibility Act of 2023, which raised the debt limit into law on June 3, 2023, ending the current debt limit crisis.[ix] On June 8, the S&P 500 rose, putting the index +20% above its October 12, 2022 low – possibly signaling the start of a new bull market.[x] A bull market is commonly defined as a +20% move in stock prices.[xi] The technology-heavy NASDAQ 100 index gained almost +40% for the first half of 2023 – its best first half ever.[xii] Crude oil regained some of May’s losses, advancing +3.8% for the month.[xiii]

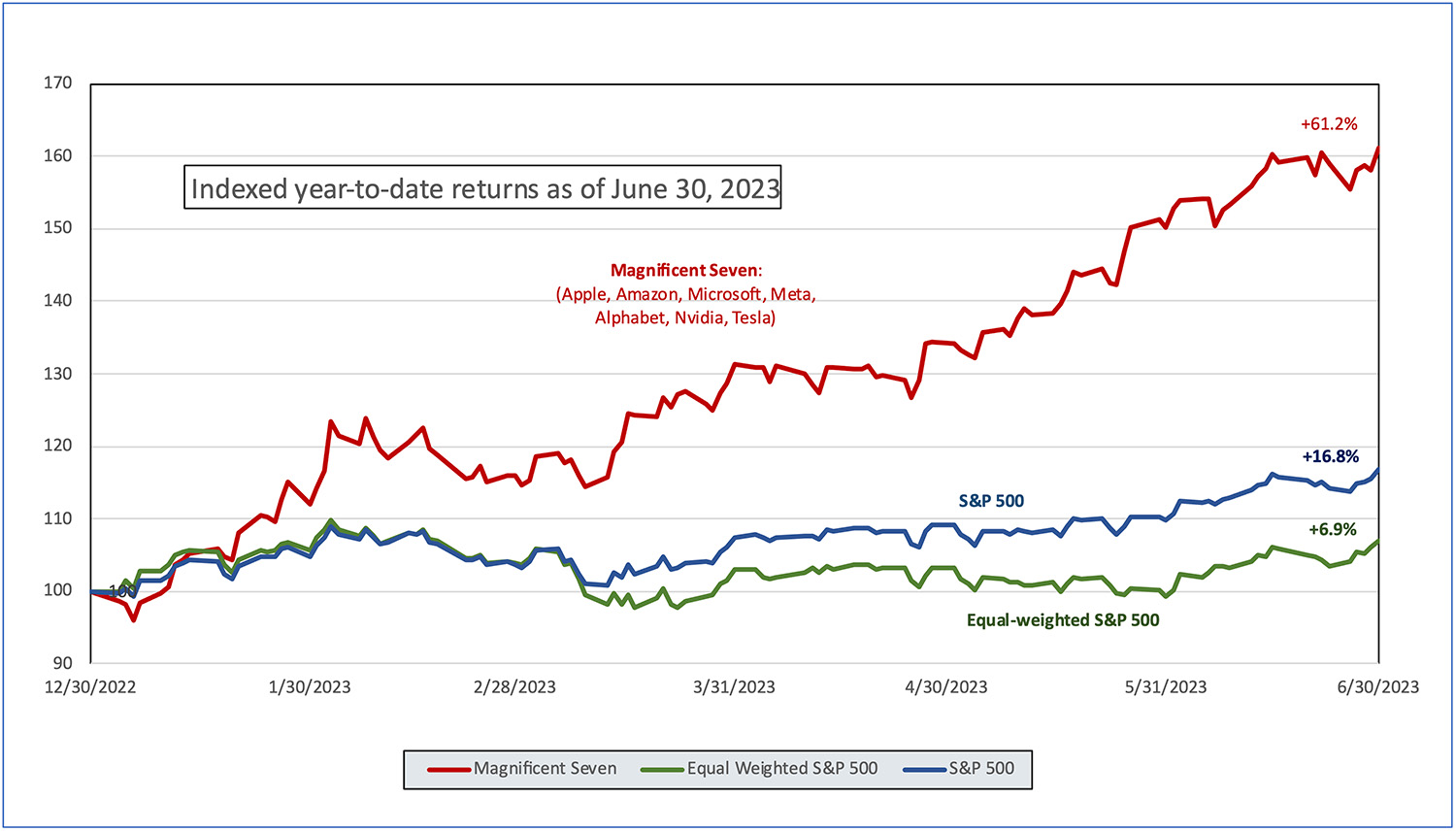

Are we in a new bull market? Technically, when measured from the October 12, 2022 low, the answer is yes. However, the recent rally in stocks has not been broad based. A small number of mega-cap technology stocks have driven returns. Michael Hartnett, investment strategist at Bank of America, has referred to the biggest seven mega-cap monopolistic U.S. tech stocks – Apple, Amazon, Microsoft, Meta, Alphabet, Nvidia and Tesla – as the Magnificent Seven.[xiv] As seen in the following chart, year-to-date through June 30, 2023, the Magnificent Seven gained +61.2%.[xv] The S&P 500, a market cap weighted index, gained +16.8%[xvi] as the equal-weighted S&P 500 was only up +6.9% during this same period.[xvii]

According to J.P. Morgan Asset Management, the top ten largest companies in the S&P 500 accounted for over 95% of the index’s year-to-date return for the first half of 2023.[xviii]

Historically, when a small number of stocks dominate overall market performance, it is not automatically a reason to sell equities. Sometimes the rally will broaden out to stocks that have lagged in performance and sometimes the outperforming stocks will give back some of their returns. While we are hopeful the current rally will broaden out to lagging stocks, we are cautious as many strategists expect a recession at some time in the next twelve months. As we wrote about last month in Technology Bubble 2.0?, it is our opinion that the current outperformance of the Magnificent Seven has been driven by artificial intelligence (A.I.) mania and we are skeptical that the gains can hold. Six of the seven Magnificent Seven stocks are experiencing sharply declining sales and earnings growth this year.[xix]

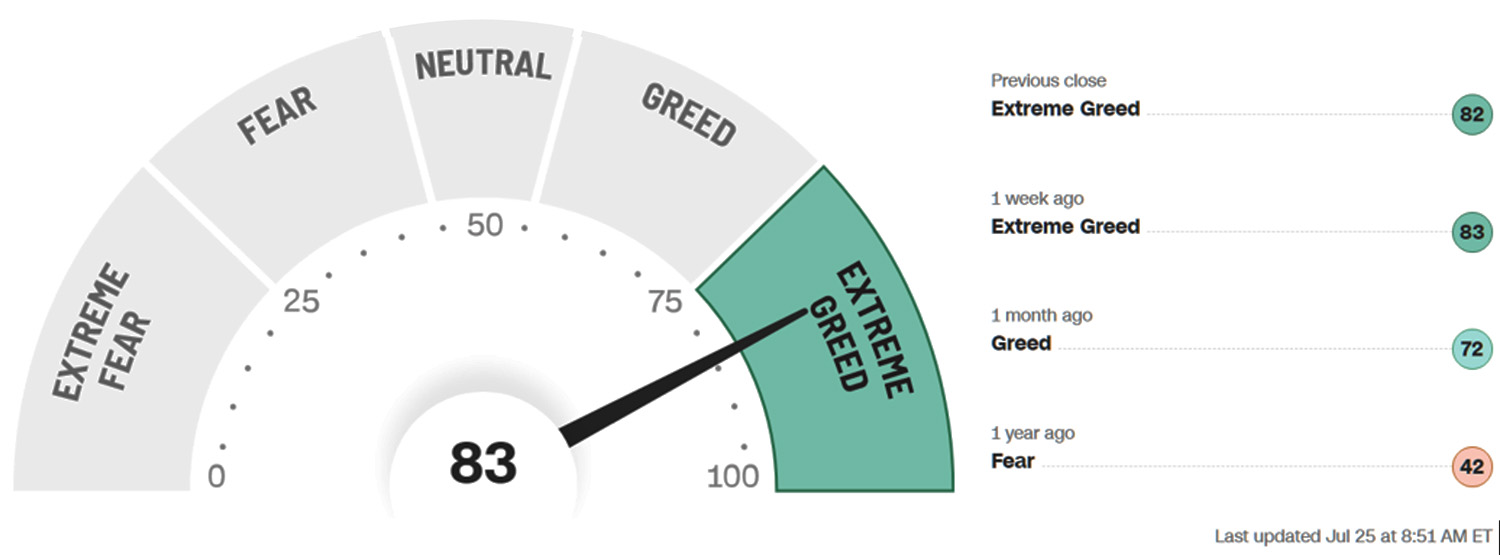

CNN’s Fear & Greed Index has reached the “Extreme Greed” level as seen in the graphic below.[xx]

Source: https://www.cnn.com/markets/fear-and-greed as of 8:53am, 7/25/2023

We agree with legendary investor Warren Buffett’s thoughts on fear and greed. Buffett, in his 1986 Berkshire Hathaway letter to shareholders famously wrote, “What we do know, however, is that occasional outbreaks of those two super-contagious diseases, fear and greed, will forever occur in the investment community. The timing of these epidemics will be unpredictable. And the market aberrations produced by them will be equally unpredictable, both as to duration and degree. Therefore, we never try to anticipate the arrival or departure of either disease. Our goal is more modest: we simply attempt to be fearful when others are greedy and to be greedy only when others are fearful.”[xxi]

Many investors currently have FOMO – fear of missing out. We believe many investors are experiencing the disease of greed and it appears dangerous to chase the returns of the Magnificent Seven stocks. Some investors have suffered in the past when they chased returns for fear of missing out. Chuck Prince, CEO of Citigroup in July 2007 was interviewed by the Financial Times regarding his company’s investment exposure and said that global liquidity was enormous and, “As long as the music is playing, you’ve got to get up and dance. We’re still dancing.”[xxii] As Prince was saying “get up and dance” in July 2007, Bear Stearns was bailing out two hedge funds with $20 billion of exposure to subprime mortgages. Many historians cite Bear Stearns as the beginning of the 2007-2008 Great Financial Crisis (GFC). During the GFC, stock markets experienced large drawdowns and it took years for investors to recover. We wrote about just how long it took markets to recover in What If the Bubble Bursts?[xxiii] Some stocks never recovered – Citigroup’s stock currently trades -90% lower than where it was in July 2007.[xxiv] Citigroup’s CEO may have better served his shareholders if he sat the dance out. Have investors already forgotten that earlier this year we experienced three of the four largest bank failures ever – First Republic Bank, Silicon Valley Bank and Signature Bank?[xxv] The Federal Reserve has not forgotten. On July 10, Michael Barr, the Federal Reserve’s Vice Chair for Supervision announced that he is advocating tougher bank capital requirements and tougher annual stress tests for U.S. banks.[xxvi] Will tougher banking requirements affect liquidity?

At CIG, we are not entirely sitting the current dance out. We are limiting our equity exposure. At the end of June 2023, our CIG Dynamic Growth Strategy held -29% less U.S. equities than the growth benchmark.[xxvii] We have taken this difference and put it into liquid alternative investments which helped us outperform the markets last year and aim to offer some protection again should markets sour in the second half of this year.

To attempt to strike the right balance in client portfolios, we think that we should be striving to reach the return necessary to meet the various needs of our clients’ financial plans while taking as little risk as possible to meet that goal. For many clients, now at mid-year, we are halfway there.

We would like to hear from you. Please reach out to Brian Lasher (BLasher@cigcapitaladvisors.com), Eric T. Pratt (EPratt@cigcapitaladvisors.com) or the rest of the CIG team.

This report was prepared by CIG Asset Management and reflects the current opinion of the authors. It is based upon sources and data believed to be accurate and reliable. Opinions and forward-looking statements expressed are subject to change without notice. This information does not constitute a solicitation or an offer to buy or sell any security.

[i] The Growth Benchmark is a blend of 60% Russell 3000, 25% MSCI All-Country ex U.S. and 15% Bloomberg U.S. Aggregate Bond indices. Sources: CIG, Zephyr, and Morningstar.

[ii] The Balanced Benchmark is a blend of 45% Russell 3000, 10% MSCI All-Country ex U.S. and 45% Bloomberg U.S. Aggregate Bond indices. Sources: CIG, Zephyr, and Morningstar.

[iii] Zephyr: S&P 500

[iv] Zephyr: Bloomberg U.S. Aggregate Bond

[v] Zephyr: MSCI EAFE Net

[vi] Zephyr: MSCI Emerging Markets Net

[vii] CIG calculated using data from finance.yahoo.com

[viii] CIG calculated using data from finance.yahoo.com

[ix] https://www.nytimes.com/2023/06/03/us/politics/biden-debt-bill.html

[x] https://www.reuters.com/markets/us/behold-wall-streets-new-bull-market-maybe-2023-06-08/

[xi] https://www.investopedia.com/terms/b/bullmarket.asp

[xii] https://twitter.com/Schuldensuehner/status/1674873071058972672

[xiii] See table above

[xiv] https://money.com/faang-magnificent-seven-tech-stocks/

[xv] The Magnificent 7 index is a market cap weighted index comprised of seven stocks – Apple, Amazon, Microsoft, Meta, Alphabet, Nvidia and Tesla – and has been calculated by CIG Asset Management using data obtained from finance.yahoo.com

[xvi] The S&P 500 is represented by SPDR S&P 500 ETF Trust (SPY) and returns have been calculated by CIG using data from finance.yahoo.com

[xvii] The equal-weighted S&P 500 is represented by Invesco S&P 500 Equal Weight ETF (RSP) and returns have been calculated by CIG using data from finance.yahoo.com

[xviii] J.P. Morgan Asset Management Weekly Market Recap, dated 07/03/2023

[xix] The High Tech Strategist newsletter dated June 28, 2023

[xx] https://www.cnn.com/markets/fear-and-greed as of July 12, 2023

[xxi] https://www.berkshirehathaway.com/letters/1986.html

[xxii] https://archive.nytimes.com/dealbook.nytimes.com/2010/04/08/prince-finally-explains-his-dancing-comment/

[xxiii] https://cigcapitaladvisors.com/cig-asset-management-review-what-if-the-bubble-bursts/

[xxiv] Calculated by CIG Asset Management using data from finance.yahoo.com

[xxv] https://www.bankrate.com/banking/largest-bank-failures/

[xxvi] https://www.federalreserve.gov/newsevents/speech/barr20230710a.htm

[xxvii] Calculated by CIG Asset Management

Image: Kameleon007/iStock

CIG Asset Management Update: Technology Bubble 2.0?

Commentary:

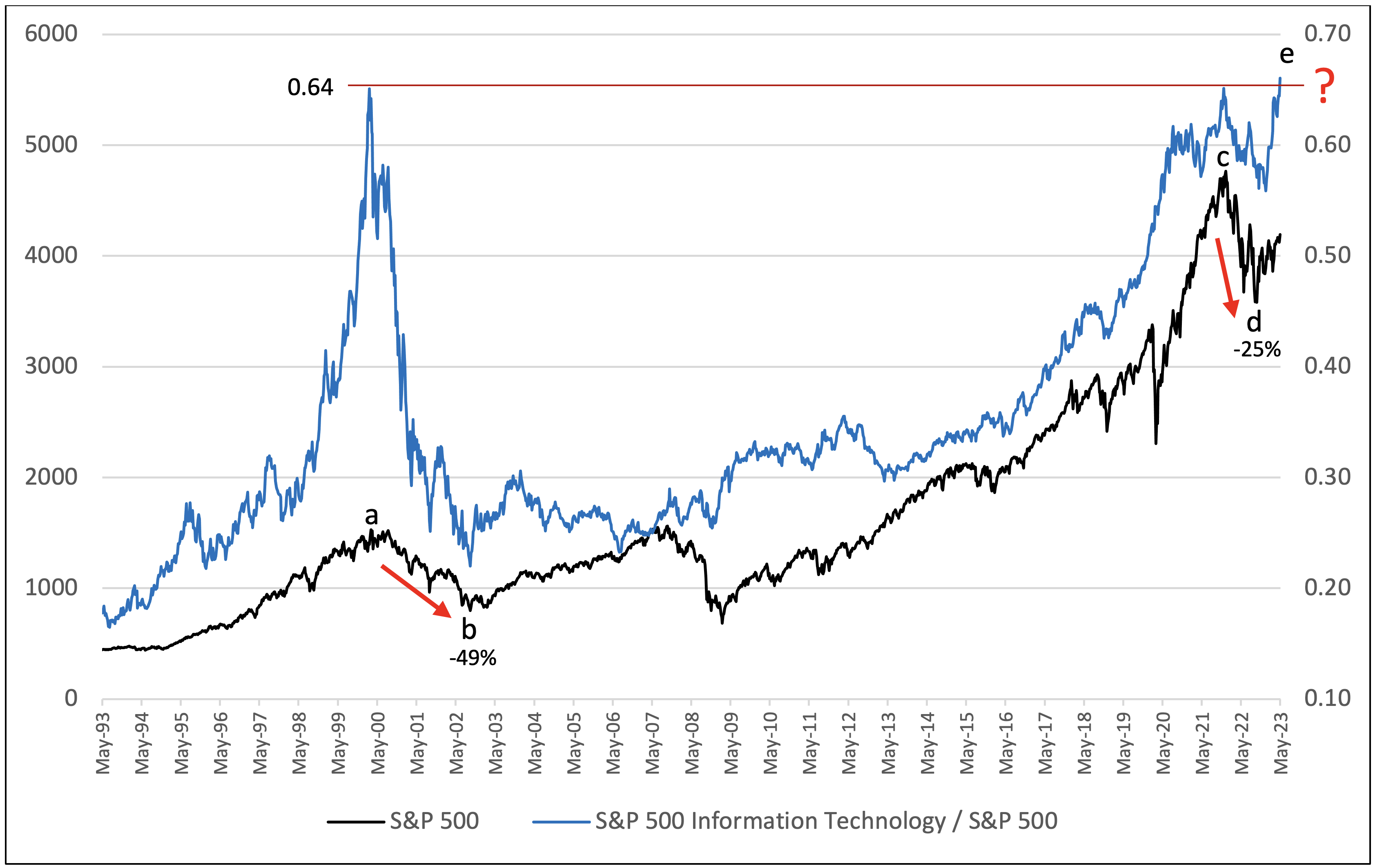

The performance ratio of the S&P 500 Information Technology Sector to the S&P 500[i] (the blue line on the above chart) has hit an all-time high of 0.66. The ratio’s previous all-time high was set in March 2000 at 0.64. As we previously discussed in What If the Bubble Bursts?, from March 27, 2000 (a) to October 9, 2002 (b) the S&P 500 (black line) fell -49% and then it took over 7 years to recover its losses after the peak. This same ratio hit 0.64 again on December 27, 2021 (c) and was followed by a -25% drawdown in the S&P 500 through October 10, 2022. (d) Now, as of May 15, 2023, this important ratio has hit a new all-time high of 0.66. (e)[ii] Will history repeat? Are we currently in a second massive technology bubble? No one knows for sure – but we are very cautious.

The rally thus far year-to-date has been narrow and concentrated in a few names. Six S&P 500 stocks – Apple, Microsoft, Nvidia, Alphabet, Amazon, and Meta – have contributed 90% of the gains of the overall index year-to-date through May 18, 2023.[iii] Five of these stocks are working on incorporating artificial intelligence (A.I.) into their business models and product offerings. While A.I. could be disruptive in the long run, the euphoria in anything A.I.-related reminds us of 1999, when many of the dot-com stocks soared in value with the internet as we know it now was still in its infancy.

Consequently, we continue to attempt to optimize our client’s exposure to the information technology sector in our pursuit of navigating our clients’ investments through these potentially turbulent market conditions. It is impossible to predict where these developments will lead, of course, but periods of upheaval can create opportunities for transformative change. We stand ready to possibly increase our allocation to domestic equities should the market rally broaden out to other sectors that have not kept up with the mega-cap growth stocks that have led year-to-date thus far. If we experience a significant market drawdown, then great opportunities could exist in the market which we would endeavor to evaluate and potentially participate in.

While volatility has moved lower over the course of 2023[iv], we do not expect that to persist for the remainder of the year. Therefore, we continue to stay the course of risk-balanced investing. We remain focused on striking the right aggressiveness versus defensiveness in client portfolios given the evolving uncertainty in the markets, the economy, and geopolitics.

Please reach out to Brian Lasher (BLasher@cigcapitaladvisors.com), Eric T. Pratt (EPratt@cigcapitaladvisors.com) or the rest of the CIG team if you have any questions.

CIG Asset Management Update October 2020: A New Hope?

Summary:

- Diversifying to include

Emerging Markets helps in tough month for Developed Markets.i,ii,iii - Continued worries

about rising COVID-19 cases and the economy.iv - Narratives appear

to be shifting as more evidence of a potential market inflexion point.

Commentary:

Globally, this month

was tough for Developed Markets and not for Emerging Markets. In October,

returns for the S&P 500 were -2.8%[i]

and MSCI EAFE was -4.1%[ii]

while the MSCI Emering Markets was +2.0%[iii].

It was the second month in a row of monthly declines in U.S. equities. As

mentioned before, we continue to employ diversification specifically to areas

like Emerging Markets to potentially cushion against U.S. equity losses as in

October.

Overall, Developed

Markets suffered from increasing COVID-19 cases[iv]

and in the U.S., diminished hopes of a pre-election stimulus package. The month

culminated with a -5.6%[v]

sell off during the last week when technology earnings missed expectations,

with Microsoft disappointing most in our opinion.

Underneath the surface of a post-election rising market

tide, the relative price movement in sectors and investing styles (Factors)

appears staggering. Our broad measures of the underlying health of the market

continue to worsen. Events happen daily that have either likely never happened

before or not happened in a long time. For example, on November 4, the Dow

Jones Transportation sector had its worst day relative to the S&P 500 since

April 2009, down almost -4%[vi]. Growth

had its best day versus Value (using Russell 1000 indices as proxies) since

January 2001 – almost 20 years![vii] In

our opinion, the market narrative appears to be that the Federal Reserve has

everything under control and that it has “got your back.” Meanwhile, we

continue to worry about how COVID-19 will affect the economy this winter given

the explosion of cases shown by the Johns Hopkins

University’s Daily COVID-19 Data in Motion.

In October, we saw

the beginnings of a narrative shift to a scenario that reminds us of 2000,

similar to what we discussed in our August update. In that market cycle, the

technology bubble was formed by companies from buying to prepare for the risk

that at the stroke of midnight on January 1, 2000 their computers would be

unable to function. In 2020, companies and individuals spent on technology to

work from home during a pandemic. In both cases, decelerating earnings occurred

once priorities shifted away from investments in technology. Last month, it

appeared that investors started to choose between decelerating and expensive

large companies versus opportunities in growing and cheaper small companies

where client portfolios have some investments. Specifically, the Russell 1000

Growth Index (large) lost -4.7%i versus the Russell 2000 Index

(small) gained 3.4%i in October. This shift is potentially bullish

for CIG’s portfolios and less so for investors indulging in passive investments[viii].

We would like to

thank our clients and friends for their continued trust and support, as well as

to respectfully encourage all to focus on the positives on Thanksgiving Day.

Obviously, 2020 has been an excruciatingly difficult year for many of us and it

continues with the contested election and the division in the country. However,

we have a newfound appreciation for going to family gatherings, restaurants and

sporting events, for more frequent phone calls with elders, and for being able

to see our children during the workday at home.

Lastly, we suggest

that you listen to the replay of our webinar “Keeping

your Financial Plans Alive Amid Chaos.” We discuss the challenges, opportunities and questions ahead

as we navigate the current and future market conditions.

This report was prepared by CIG Asset Management and reflects the current opinion of the authors. It is based upon sources and data believed to be accurate and reliable. Opinions and forward-looking statements expressed are subject to change without notice. This information does not constitute a solicitation or an offer to buy or sell any security.

SOURCES:

[i]

Yahoo Finance

[ii] https://www.msci.com/end-of-day-data-search

[iii] https://www.msci.com/end-of-day-data-search

[iv] https://coronavirus.jhu.edu/covid-19-daily-video

[v]

Calculated by CIG using data from Yahoo Finance for 10/23 to 10/30.

[vi]

Research report from Epsilon Theory, “The King is Dead. Long Live the King”

dated 11/5/20.

[vii]

Research report from Epsilon Theory, “The King is Dead. Long Live the King”

dated 11/5/20.

[viii]

While small companies as measured by the Russell 2000 small-cap index has had

six 10%+ multi-day moves in 2020, per Bespoke Investment Group, the number of

underlying companies with negative profits appears to be quite large relative

to history and could pose a problem if investors just buy the index versus

those stocks which have positive earnings.

Managing a Healthcare Practice through the Pandemic: Finance and Operation

Medical practices, dental practices, small and rural hospitals and larger healthcare systems alike are feeling the effects of the COVID-19 pandemic. Recent regulatory changes, like the $8.3 billion emergency funding measure that expands Medicare reimbursements for telemedicine and the prohibition of all non-essential medical, surgical, and dental procedures during the outbreak, have upended the planned revenue cycle of nearly every U.S. healthcare practice or business. How can medical practice owners, dental practice owners and other healthcare managers adjust the financial and operational levers of their business to better weather the economic turmoil caused by the pandemic?

Financial steps to take:

- Put together a 12-week cash flow statement to understand better how you can manage the disruption, assessing what should be coming in and what you must pay and can delay paying, including evaluating the best approach to manage your staff given the circumstances.

- Billing staff should work remotely in order to continue billing as usual and connect with insurance companies. Their time should be used to follow-up on past billings and accounts receivables.

- Reach out to your bank to determine if/when you can setup or increase a line of credit for your business.

- Contact your accountant for up-to-date financials and clarity regarding whether you will be paying your sales/use and withholdings taxes as normal or taking advantage of your state’s relief, if applicable.

- Look for state and federal programs you may qualify for, including the SBA’s Economic Injury Disaster Loans.

Operational steps to take:

- Consider employees carefully. Can non-essential staff work remotely or even be laid off or furloughed to find work elsewhere through a healthcare staffing company, given that many large systems are currently understaffed? Use web conferencing to hold staff meetings, utilizing services such as Zoom, WebEx, Skype, Google Hangouts and/or FaceTime.

- Move to telehealth when possible, as CMS changes are allowing increased telehealth reimbursements. Using video visits for patients with compromised health can help them avoid coronavirus exposure. Chronic medicine can be delivered to patients’ homes. Of course, when moving to telehealth solutions, notification to patients and training staff members is necessary.

- Prepare for patient visits by securing the doors and screening patients before entry. Provide hand sanitizer, face masks, and gloves and take basic sanitary precautions that can make a difference:

- Disinfect all surfaces, equipment and door knobs between patient consults.

- Shared resources should be kept clean.

- Proper hand hygiene.

- Waiting-room chairs are placed six feet apart and social distancing respected during interactions as possible; alternatively, you can allow sign-in/call-in at the entrance/via phone and ask patients to stay in their car in the parking lot and call them when you are ready to take them back.

- Deal with elective procedures by rescheduling to a later date. Serve patients when you believe it medically irresponsible to delay but disclose the risks, and keep them separate from patients coming in for non-elective procedures. Please note the difference between necessary elective procedures and not-necessary elective procedures.

- Update your website and phone greetings to communicate your current processes and availability.

Medical practices, dental practices, and small and rural hospitals are more likely to weather the pandemic storm by taking positive financial and operational steps now to mitigate business losses and emerge from the crisis in an even-stronger market position. For individual steps your medical or dental practice or hospital should take, schedule a complimentary phone consultation here or join our webinar, “Managing a Healthcare Practice through the Pandemic: Finance and Operations” on Thursday, April 2 at 12:30 p.m. by registering here.