CIG Asset Management Update: Where are we now?

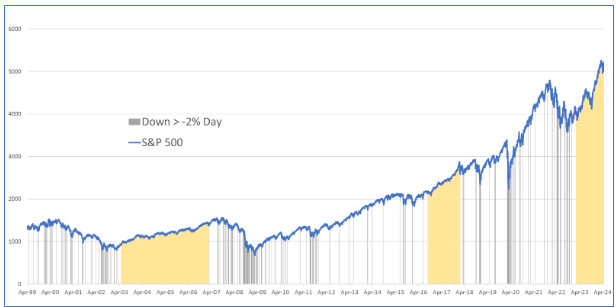

The S&P 500 currently is experiencing its third longest period in the past 25 years without a single-day decline of over 2%. Yes, including last month. The graph below depicts the past 25 years, highlighting every day when the S&P 500 fell over 2% (indicated by black vertical lines). These occurrences aren’t rare.

Chart by CIG Asset Management using data from barchart.com

The mustard-colored shaded areas represent extended periods without a 2% down day. The first yellow shaded area, 1,380 days, (from May 20, 2003, to February 27, 2007) coincided with Freddie Mac’s announcement that they would no longer buy sub-prime mortgages. [i] This marked the beginning of the great financial crisis, leading to a significant stock market drawdown over the next two years. The second longest period was 511 days, (September 12, 2016, to February 1, ) This calm period in the market ended with what became known as Volmaggedon – an event where many structured products that bet against stock market volatility lost over 90% of their value. [ii] The most recent shaded area began on February 21, 2023, and continues beyond May 9, . (443 days as of this writing) [iii] Notably, despite the S&P 500 falling -4.1% in April 2024, we still didn’t experience a single -2% down day.[iv] History teaches us that long quiet periods can often precede sudden volatility and drawdowns.

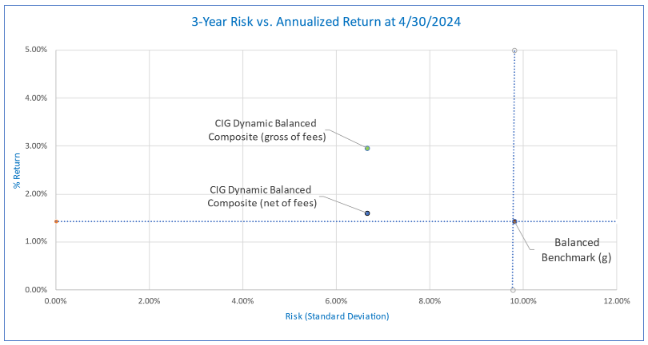

While no one can predict the future, we are currently taking less risk than the benchmarks in our managed strategies. The following chart shows the risk/return of the CIG Dynamic Balanced Composite versus the balanced benchmark for the three-year period ending April 30, 2024. Gross of fees, the balanced composite captured 207% of the benchmark’s return while only taking 68% of the Balanced Benchmark’s risk, as measured by standard deviation of returns over that 3-year period. Net of fees, the balanced composite captured 113% of the benchmark’s return. [v]

CIG Asset Management, Tamarac

The graph above illustrates the performance of the CIG Dynamic Balanced Composite over the past three years. Specifically, the annualized return of this strategy is above the horizontal dotted blue line which represents the annualized return of the balanced benchmark. Additionally, the strategy’s risk level is to the left of the vertical dotted blue line, which corresponds to the balanced benchmark’s risk. This positioning indicates good diversification: achieving higher returns than the benchmark while assuming less risk. However, achieving this balance isn’t easy, especially in a potentially euphoric market, and requires careful decision-making and strategic asset allocation.

Why are we focused on risk and what are we trying to avoid? Prolonged Downturns. Consider this graph, which first appeared in our update titled ‘What if the Bubble Bursts?’ on November 8, 2021.

CIG Asset Management, barchart.com

Imagine an investor who put their money in the S&P 500 on March 27, 2000—the peak of the dot-com boom. They would have waited 7 years to break even by May 21, 2007. Briefly, there was a window to exit and remain whole until October 31, 2007. Then came the Great Financial Crisis, requiring another 5 plus years to recover by March 4, 2013. [vi]Our Question for Investors – Are you comfortable waiting 5, 7, or even close to 13 years to break even? For those nearing retirement or relying on investments for living expenses, the answer is likely no. While this period was extraordinary, it wasn’t that long ago. And now, the AI bubble appears to have striking similarities to the dot-com era. As of April 22,2024, the information technology sector was 30.3% of the S&P 500, nearing the dot-com record of 34.8% in March 2000. [vii]

At CIG, we take a thoughtful and balanced approach to investment management. As we navigate the ever-changing economic and geopolitical landscape, our outlook remains cautiously optimistic. In this phase of the market cycle, our primary goal is to achieve returns that align with our clients’ diverse financial plans while minimizing risk. We draw inspiration from Benjamin Graham’s wisdom in his book, The Intelligent Investor. “The best way to measure your investing success is not by whether you’re beating the market but by whether you’ve put in place a financial plan and a behavioral discipline that are likely to get you where you want to go. In the end, what matters isn’t crossing the finish line before anybody else but just making sure that you do cross.”

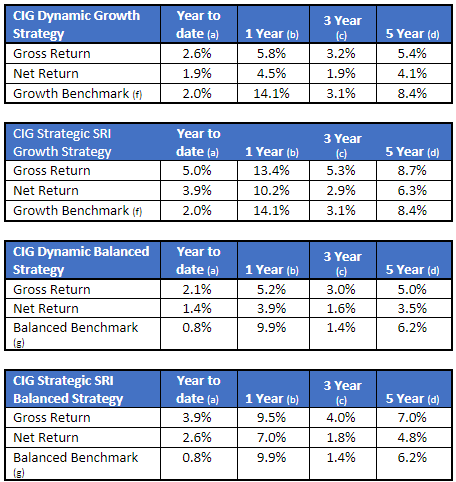

Strategy Returns as of 4/30/2024:

Performance has been attested to by ACA Group for the period August 1, 2018, through December 31, 2022.

Strategy returns are calculated independently on a daily basis and linked geometrically to produce a monthly return. Total investment performance includes realized and unrealized gains and losses, dividends, and interest. Accrual accounting is used to record interest income while dividends are recorded on a cash basis. Trade date accounting is used for calculation and valuation purposes.

Past performance is not indicative of future results.

(a) Represents performance from January 1, 2024, through April 30, 2024.

(b) Represents performance from May 1, 2023, through April 30, 2024.

(c) Represents annualized performance from May 1, 2021, through April 31, 2024.

(d) Represents annualized performance from May 1, 2019, through April 31, 2024.

(f) The Growth Benchmark is a blend of 60% Russell 3000, 25% MSCI All-Country World ex US and 15% Bloomberg US Aggregate Bond indices.

(g) The Balanced Benchmark is a blend of 45% Russell 3000, 10% MSCI All-Country World ex US and 45% Bloomberg US Aggregate Bond indices.

[i] https://fraser.stlouisfed.org/title/freddie-mac-5132/freddie-mac-announces-tougher-subprime-lending-standards-help-reduce-risk-future-borrower-default-518857

[ii] https://rpc.cfainstitute.org/en/research/financial-analysts-journal/2021/volmageddon-failure-short-volatility-products

[iii] Calculated by CIG Asset Management using data from barchart.com

[iv] Calculated by CIG Asset Management using data from finance.yahoo.com

[v] Calculated by CIG Asset Management using data from Tamarac

[vi] Calculated by CIG Asset Management using data from barchart.com

[vii] https://www.investopedia.com/best-25-sp500-stocks-8550793, https://www.bespokepremium.com/interactive/posts/think-big-blog/historical-sp-500-sector-weightings

CIG Asset Management Update: The Stock Market Rally May Be Broadening

In October 2023, we shared the CIG Asset Management Update: Year-to-Date U.S. Stock Performance in Pictures and we discussed how the Magnificent 7[i], seven mega-cap growth stocks, were driving the returns of the S&P 500.

This outperformance continued through year end as you can see in the December 31, 2023 FinViz heat map below.

Source: FinViz as of 12/31/2023

In the year, 2023, the Magnificent 7 stocks experienced an average return of +111% while the S&P 500 Index only gained +26%. The Equal-Weighted S&P 500 Index only gained +12%. If you removed the Magnificent 7 stocks from the Equal-Weighted S&P 500 Index, you would have only gained +8%. [ii]

The strong performance of the Magnificent 7 stocks has extended into 2024. As of February 29, 2024, these seven stocks have gained +12.7%, outpacing the S&P 500’s increase of +7.1% and the Equal-Weighted S&P 500 Index’s gain of +3.2%.[iii]

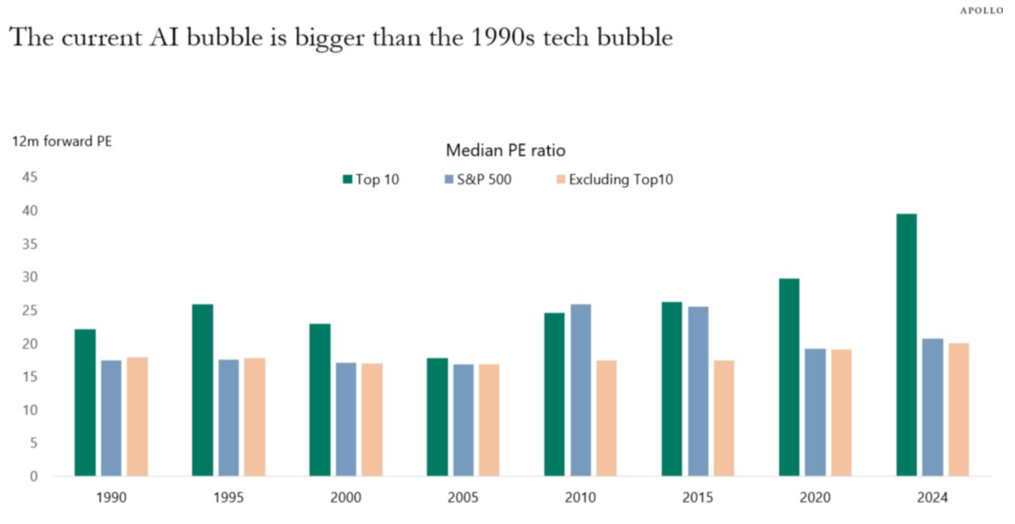

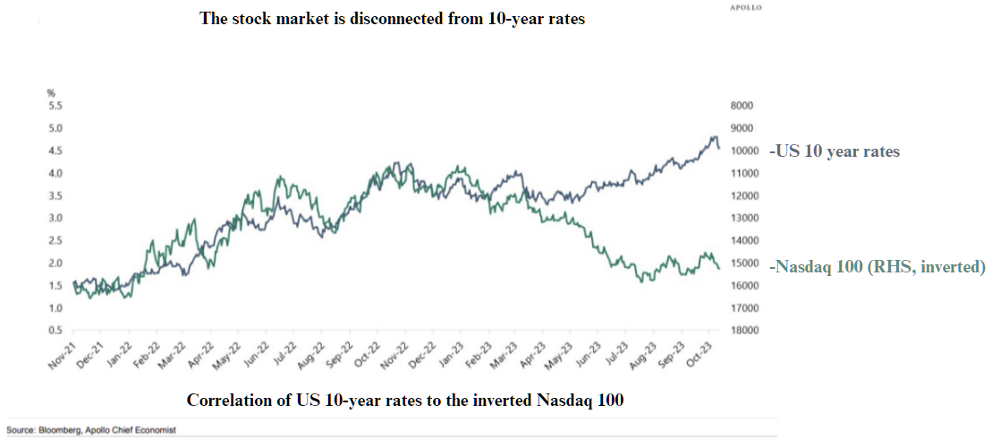

We believe the Magnificent 7 stocks are currently trading at levels considered expensive compared to historical standards. Torsten Slok, Apollo’s Chief Economist, has recently showed that when you compare the median 12-month forward price-to-earnings (PE) ratio of the top ten companies in the S&P 500, which include all of the Magnificent 7 stocks, they are much more expensive now than they were during the tech bubble of the 1990s. [iv]

Source:Bloomberg, Apollo Chief Economist. Note: Data as of January 31, 2024.

With that being said, we are seeing some encouraging signs that the stock market rally may finally be starting to broaden out. For the week ended 3/6/2024, we saw four of the Magnificent 7 stocks; Microsoft (MSFT), Apple (AAPL), Alphabet (GOOG), and Tesla (TSLA) move lower as many other stocks outside of the technology sector rose. You can see this in the March 6, 2024 FinViz heat-map below.

Source: FinViz as of 3/6/2024

While we find it encouraging to see a wider equity market participation, we still believe strongly in the value of diversification. Diversification is not supposed to maximize returns, it is designed to reduce investment risk. A diversified portfolio at times won’t keep up with the market when the bulk of returns are concentrated in a small group of stocks like the Magnificent 7. We strive to diversify our investments amongst industries and sectors, size (large-cap and small-cap), geography, growth versus value and alternative asset classes. Some of these investments are negatively correlated to the stock market – what that means is historically when the stock market traded lower – these investments gained in value. Past performance is not a guarantee of future results, but history helps guide us.

At CIG, we believe in risk-balanced investing. We believe investors should consider how much risk they are taking to achieve returns. We think that we should be striving to reach the return necessary to meet the various needs of our client’s financial plans while, at this point in the market cycle, taking as little risk as possible to meet that goal. We want you to sleep at night.

Please reach out to Brian Lasher (blasher@cigcapitaladvisors.com), Eric T. Pratt (epratt@cigcapitaladvisors.com) or the rest of the CIG team.

This report was prepared by CIG Asset Management and reflects the current opinion of the authors. It is based upon sources and data believed to be accurate and reliable. Opinions and forward-looking statements expressed are subject to change without notice. This information does not constitute a solicitation or an offer to buy or sell any security.

[i] The Magnificent 7 stocks are: Apple (AAPL), Microsoft (MSFT), Alphabet (GOOGL), Amazon.com (AMZN), Nvidia (NVDA), Tesla (TSLA), and Meta Platforms (META)

[ii] https://www.forbes.com/sites/greatspeculations/2024/01/22/2023-in-review/?sh=78aab8bd690b

[iii] Calculated by CIG Asset Management for the Roundhill Magnificent Seven ETF (MAGS) using data from finance.yahoo.com

[iv] The Daily Spark, February 25, 2024 – Apollo Academy

Update from CIG Asset Management – Wealth Destroyer – As Seen On TV

CNBC television frequently has a guest, Cathie Wood, Founder & CEO of ARK Invest. Oftentimes Cathie will tout the funds and stocks that are held in the funds she manages. On April 12, 2022, Cathie Wood said the following live on CNBC, “Over the next five years we’re expecting a 50% compound annual rate of return for the next five years.” [i]

How has the performance of ARK Invest’s Flagship Fund, the ARK Innovation ETF (ARKK), been since her bold statement in April 2022? As seen in the chart below, the shaded area representing ARKK shows a decline of -21.2% from April 12, 2022, to February 7, 2024! In contrast, the S&P 500 has gained+13.6% over this same period! [ii]

The current performance of ARRK, as indicated in the chart above, doesn’t appear to align with the 50% rate of return forecasted in her April 2022 statement. Cathie has made multiple appearances on CNBC since April 2022, and two of her latest appearances have caught our attention.

On January 23 ,2024, Cathie discussed Bitcoin ETFs and said, “This is one of the most important investments of our lifetime.” [iii] This was only 12 days after ARK Invest launched the ARK 21shares Bitcoin ETF (ARKB). [iv] ARKB has fallen -11.7% since its launch on January 11, 2024, to February 7, 2024. Bitcoin itself only fell -5.0% during that same period. A cryptocurrency investor lost over twice as much owning ARKB versus Bitcoin itself during this period of time! [v]

On February 7, 2024, Cathie appeared on CNBC’s program “Last Call”. Cathie spoke about Tesla and said, “Robo-taxis are a software as a service model” and that “EVs will be the bulk of the auto market in the next 5 years.” [vi] As of February 8, 2024, Tesla is ARKK’s second largest holding. [vii] Tesla is down -25% year-to-date as of February 7, 2024. [viii]

As you read this you may be thinking, “CIG is being very critical of Cathie Wood and her ARK Funds.” We at CIG are not alone in our criticism. Morningstar recently published a report- “15 Funds That Have Destroyed the Most Wealth Over the Past Decade”. According to Amy C. Arnott, CFA and author of the report, “The ARK family wiped out an estimated $14.3 billion in shareholder value over the 10-year period—more than twice as much as the second-worst fund family on the list. ARK Innovation alone accounts for about $7.1 billion of value destruction over the trailing 10-year period.”[ix] More importantly, this is not about Cathie Wood or ARK rather about objective data analysis versus media coverage.

We urge our clients and all investors to refrain from being swayed by the hype seen on CNBC or encountered while browsing the internet. Some guests on these platforms are “talking their book”, meaning they are trying to drum up interest in the investment that they already own, such as Tesla, as highlighted earlier. They also may offer the hope of beating the market or make grand predictions about their future performance similar to Cathy’s 50% comment. Instead, we ask investors to listen to the sage advice of Benjamin Graham, as the “father of value investing” and mentor to Warren Buffett. [x] In his book, “The Intelligent Investor” Graham wrote the following:

“The best way to measure your investing success is not by whether you’re beating the market but by whether you’ve put in place a financial plan and a behavioral discipline that are likely to get you where you want to go.”[xi]

The guests on financial channel talk shows tend to highlight their successes from the previous year and the promising opportunities they foresee for the current year, yet they often overlook discussing their less-than-successful experiences in 2022. Retail investors also occasionally exhibit this behavior. We counsel investors to understand what they are invested in – usually a diversified portfolio – and measure their results with the appropriate diversified, blended benchmark and how they are doing versus their financial plan. The rest is just noise.

Please reach out to Brian Lasher (blasher@cigcapitaladvisors.com), Eric T. Pratt (epratt@cigcapitaladvisors.com) or the rest of the CIG team.

This report was prepared by CIG Asset Management and reflects the current opinion of the authors. It is based upon sources and data believed to be accurate and reliable. Opinions and forward-looking statements expressed are subject to change without notice. This information does not constitute a solicitation or an offer to buy or sell any security.

[i] https://www.cnbc.com/video/2022/04/12/ark-invest-ceo-cathie-wood-says-she-expects-50-percent-compound-annual-rate-of-return-for-the-next-five-years.html

[ii] Data and chart from barchart.com

[iii] https://www.cnbc.com/video/2024/01/23/cathie-wood-on-bitcoin-etf-this-is-one-of-the-most-important-investments-of-our-lifetime.html

[iv] https://www.prnewswire.com/news-releases/the-ark-21shares-bitcoin-etf-arkb-is-available-now-302031988.html

[v] Calculated by CIG Asset Management using data from finance.yahoo.com.

[vi] https://www.cnbc.com/video/2024/02/07/ark-invest-ceo-cathie-wood-evs-will-be-the-bulk-of-the-auto-market-in-the-next-5-years.html

[vii] ARK Invest holdings data as of February 8, 2024

[viii] Calculated by CIG Asset Management using data from finance.yahoo.com.

[ix] “15 Funds That Have Destroyed the Most Wealth Over the Past Decade” – published by Morningstar 2/2/2024

[x] https://www.investopedia.com/terms/b/bengraham.asp#toc-notable-accomplishments

The Intelligent Investor, Benjamin Graham

[xi] The Intelligent Investor, Benjamin Graham, https://www.arborinvestmentplanner.com/quotes-from-the-intelligent-investor-revised-edition/ p.220

CIG Press Release: CIG Capital Advisors Announces New Advisory Board as They Posture for Growth in 2024

Contact: Joan Frank

Tel: (248) 330-0001

Email: joan@bfrankcommunications.com

www.bfrankcommunications.com

FOR IMMEDIATE RELEASE:

November 29, 2023 — Southfield, MI —CIG Capital Advisors is gearing up for major strategic growth in the upcoming years, starting with the introduction of its new CIG Advisory Board, which will play a pivotal role in advising and shaping the company’s strategic direction and future growth.

A leading independent wealth management and business advisory services firm, CIG has recruited a distinguished group of thought leaders and innovators to serve on this board, including experts in health care, financial services, investment, and international management to enrich and elevate services for the firm’s expanding client base.

The Advisory Board members include:

- Dr. Mark Kelley, MD – Chair – Former chief executive officer, Henry Ford Medical Group and senior lecturer at Harvard Medical School

- Osman Minkara – Founder and chief executive officer at CIG Capital Advisors

- Jeff Davidson – Former head of investment at Taubman Family Office and senior consultant

- Nigel Thompson – Former president and chief executive officer, Yazaki North America

- Dina Richard – Senior vice president, treasurer and chief investment officer at Trinity Health

- Dr. Raza M. Khan, MD, FACS – Senior partner at Uropartners

- Mindy Richards – Embedded health care consultant and CEO of ChangeScape, Inc.

- Dr. Samer Y. Kazziha, MD, FACC – Senior and head of Cardiovascular Consultants P.C.

The expertise of the Advisory Board will be invaluable in growing CIG’s specialized wealth management and business advisory solutions for successful entrepreneurs and senior executives. The Advisory Board will enhance CIG’s ability to deliver strategic thinking and innovative approaches to a broad range of clients looking to grow their professional or personal wealth opportunities.

“We are honored to welcome these accomplished individuals to our Advisory Board,” said Osman Minkara, founder and CEO of CIG Capital Advisors. “Their guidance and insights will be invaluable as we continue to innovate, grow, and adapt to the ever-changing wealth management and business advisory landscape. We believe that their collective wisdom will help us steer CIG toward new horizons.”

That dedication to excellence is embraced by the Advisory Board, underscoring CIG’s determination to further expand its leadership in the financial industry. “As advisory board members, our mission is to drive innovation and bring about positive change through collective expertise and collaboration,” says Dr. Mark Kelley. “We aim to stay ahead of the curve by anticipating trends and proactively addressing challenges.”

CIG Capital Advisors has built robust integrated services that elevate the client experience. Serving as their clients’ trusted partner, CIG is committed to providing unique solutions to complex problems and to guiding clients on their individualized financial journeys. That forward thinking will drive the firm’s growth in the years ahead, as they offer robust guidance and expertise with the same personalized attention that sets CIG apart from the crowd.

About CIG Capital Advisors

Founded in 1997, CIG Capital Advisors (CIG) is a wealth management and business advisory services firm serving high-net-worth clients—enabling these individuals and families to focus on what is most important to them. CIG tailors its delivery of service based on the situation, goals, and aspirations of each client it works with. The firm seeks to provide exceptional client benefit through its independent, objective, and transparent strategic thinking and implementations. CIG is based in Southfield, MI.

For more information on CIG Capital Advisors visit cigcapitaladvisors.com. Media inquiries contact Joan Frank at B. Frank Communications at (248) 330-0001 or joan@bfrankcommunications.com.

Advisory Board

Image: Conny Schneider/Unsplash

CIG Asset Management Update: Year-to-Date U.S. Stock Performance in Pictures

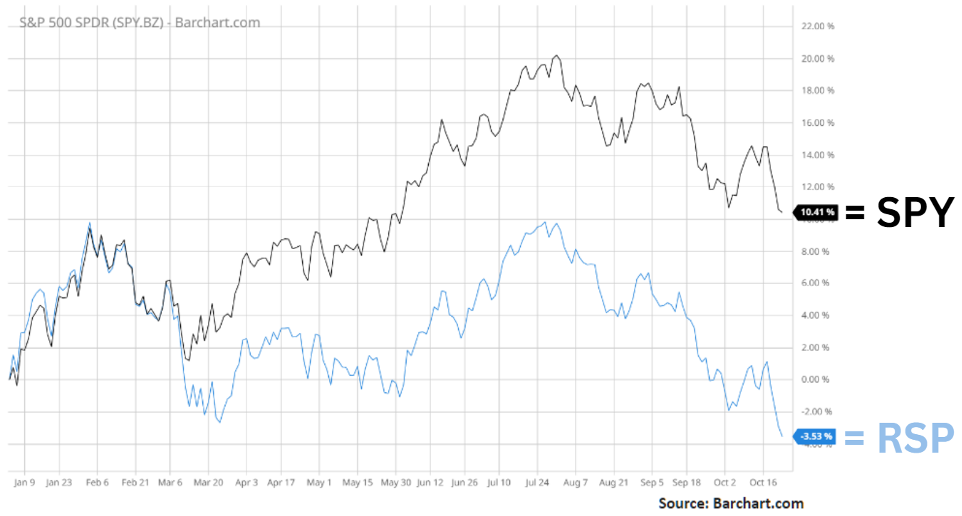

The chart below shows the year-to-date performance through October 20, 2023, of the market cap-weighted S&P 500 – represented by the SPDR S&P 50 ETF (SPY) gaining +10.4% versus the equal-weighted S&P 500 – represented by the Invesco S&P 500 Equal Weight ETF (RSP) falling -3.5%. [i]

Source: Barchart.com

Why is there such a big difference in returns between the two indices?

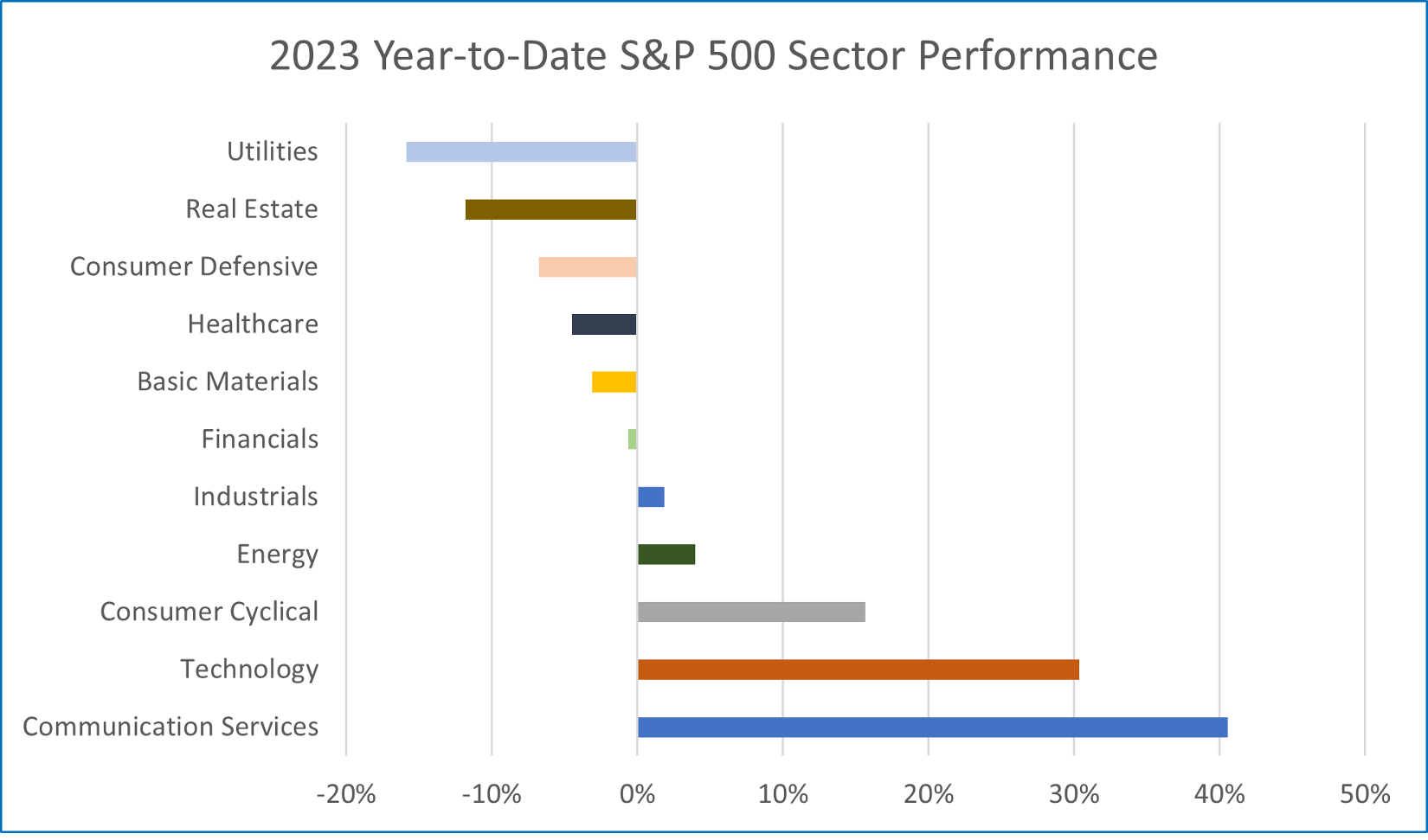

Year-to-date through October 24, 2023, the performance of the stock market and its 11 major S&P sectors may best be described as the battle between the “haves” and the “have nots”.

Three sectors, Communication Services, Technology, and Consumer Cyclicals are outperforming the other eight by a wide margin. As seen in the chart below, six sectors are down year-to-date.

Source: FinViz.com as of October 24, 2023

What is driving the performance of the three outperforming sectors? Why is performance so skewed?

The answer to why there is such a big difference in returns between the equal-weighted S&P 500 and the size-weighted S&P 500 and in returns between sectors lies in this heat map which shows all 500 companies that are included in the S&P 500. [ii]

Source: FinViz.com as of October 24, 2023

The answer lies with the seven large bright green boxes with their symbols circled in yellow. All seven of these stocks are in one of the three outperforming sectors previously identified on the S&P 500 Sector Performance bar chart. Bank of America analyst Michael Hartnett has called this group of seven stocks the “Magnificent 7”.[iii] Currently, over 25% of the S&P 500’s total market capitalization is in these Magnificent 7 stocks. [iv]

According to Torsten Slok, Chief Economist at Apollo Asset Management, “The bottom line is that returns this year in the S&P 500 have been driven entirely by returns in the seven biggest stocks, and these seven stocks have become more and more overvalued.”[v] Apollo Asset Management manages over half a trillion dollars in assets.

Why is this so remarkable and when will this situation end?

Slok concludes that “tech valuations are very high and inconsistent with the significant rise in long-term interest rates… In short, something has to give. Either stocks have to go down to be consistent with the current level of interest rates. Or long-term interest rates have to go down to be consistent with the current level of stock prices.”[vi]

Year-to-date through September 30, if you invested in a DIVERSIFIED portfolio with 60% invested in the Equal Weighted S&P 500 (RSP) and 40% invested in Bloomberg Barclay Aggregate Bond Index (AGG), you would have generated lower returns than if one chased only these Magnificent 7 stocks. [vii]

Some investors might describe us at CIG as being bearish because we don’t find the Magnificent 7 attractive, but we’re not so pessimistic as to believe there are only seven growth opportunities in the entire global equity market. In particular, we feel that we have identified an investment theme for long-term investors.

We are beginning to allocate money into Clean Transition Investing – a theme where one invests in different areas that work towards net zero emissions, or clean energy. The Paris Agreement of 2015 outlined the long-term goal of reaching net zero emissions by the year 2050.[viii] Fixing the electrical grid, focusing on renewable energy, hydrogen, energy storage, electric vehicles and the required infrastructure that goes along with them, sustainable mining, and smart agriculture are just examples of what need to be worked on.

While the eventual changing of sector leadership across cycles tends to be accompanied by significant market volatility, we will be there to guide you through these changes. CIG’s goals are to provide a financial roadmap for our clients and their families – over both near-term and long-term time horizons – as we implement structures to potentially increase protection of your assets and optimize investment risks and returns, and aid in the creation of legacy platforms.

We would welcome a conversation with you regarding how we can help you navigate these interesting times. We would like to hear from you. Please reach out to Brian Lasher (blasher@cigcapitaladvisors.com), Eric T. Pratt (epratt@cigcapitaladvisors.com) or the rest of the CIG team.