CIG in the News: MedCityNews, “Why now is a good time to consider exit strategies for your practice”

The coronavirus pandemic has been a catalyst, both supercharging the investment demand for physician practices and accelerating the consolidation trend in the healthcare industry. With strong sale prices on an upward trend, CIG Capital Advisors discusses in MedCity News what physician-owned practices should know before considering a deal.

Why now is a good time to consider exit strategies for your practice

Independent practices are grappling with increasing technology costs, regulatory requirements, and tighter margins and now may be an opportune time to consider exiting.

As the financial and emotional stress caused by the Covid-19 pandemic drags on, many physician-owners are taking a hard look at their professional — and personal — priorities. For some, that means finally moving forward on plans to exit their practice. Despite the turmoil and uncertainty, now may be an opportune time to make a move. Read more here.

For a confidential consultation with a CIG Capital Advisors medical practice advisor, email Brian Lasher.

CIG Asset Management Update October 2020: A New Hope?

Summary:

- Diversifying to include Emerging Markets helps in tough month for Developed Markets.i,ii,iii

- Continued worries about rising COVID-19 cases and the economy.iv

- Narratives appear to be shifting as more evidence of a potential market inflexion point.

Commentary:

Globally, this month was tough for Developed Markets and not for Emerging Markets. In October, returns for the S&P 500 were -2.8%[i] and MSCI EAFE was -4.1%[ii] while the MSCI Emering Markets was +2.0%[iii]. It was the second month in a row of monthly declines in U.S. equities. As mentioned before, we continue to employ diversification specifically to areas like Emerging Markets to potentially cushion against U.S. equity losses as in October.

Overall, Developed Markets suffered from increasing COVID-19 cases[iv] and in the U.S., diminished hopes of a pre-election stimulus package. The month culminated with a -5.6%[v] sell off during the last week when technology earnings missed expectations, with Microsoft disappointing most in our opinion.

Underneath the surface of a post-election rising market tide, the relative price movement in sectors and investing styles (Factors) appears staggering. Our broad measures of the underlying health of the market continue to worsen. Events happen daily that have either likely never happened before or not happened in a long time. For example, on November 4, the Dow Jones Transportation sector had its worst day relative to the S&P 500 since April 2009, down almost -4%[vi]. Growth had its best day versus Value (using Russell 1000 indices as proxies) since January 2001 – almost 20 years![vii] In our opinion, the market narrative appears to be that the Federal Reserve has everything under control and that it has “got your back.” Meanwhile, we continue to worry about how COVID-19 will affect the economy this winter given the explosion of cases shown by the Johns Hopkins University’s Daily COVID-19 Data in Motion.

In October, we saw the beginnings of a narrative shift to a scenario that reminds us of 2000, similar to what we discussed in our August update. In that market cycle, the technology bubble was formed by companies from buying to prepare for the risk that at the stroke of midnight on January 1, 2000 their computers would be unable to function. In 2020, companies and individuals spent on technology to work from home during a pandemic. In both cases, decelerating earnings occurred once priorities shifted away from investments in technology. Last month, it appeared that investors started to choose between decelerating and expensive large companies versus opportunities in growing and cheaper small companies where client portfolios have some investments. Specifically, the Russell 1000 Growth Index (large) lost -4.7%i versus the Russell 2000 Index (small) gained 3.4%i in October. This shift is potentially bullish for CIG’s portfolios and less so for investors indulging in passive investments[viii].

We would like to thank our clients and friends for their continued trust and support, as well as to respectfully encourage all to focus on the positives on Thanksgiving Day. Obviously, 2020 has been an excruciatingly difficult year for many of us and it continues with the contested election and the division in the country. However, we have a newfound appreciation for going to family gatherings, restaurants and sporting events, for more frequent phone calls with elders, and for being able to see our children during the workday at home.

Lastly, we suggest that you listen to the replay of our webinar “Keeping your Financial Plans Alive Amid Chaos.” We discuss the challenges, opportunities and questions ahead as we navigate the current and future market conditions.

This report was prepared by CIG Asset Management and reflects the current opinion of the authors. It is based upon sources and data believed to be accurate and reliable. Opinions and forward-looking statements expressed are subject to change without notice. This information does not constitute a solicitation or an offer to buy or sell any security.

SOURCES:

[i] Yahoo Finance

[ii] https://www.msci.com/end-of-day-data-search

[iii] https://www.msci.com/end-of-day-data-search

[iv] https://coronavirus.jhu.edu/covid-19-daily-video

[v] Calculated by CIG using data from Yahoo Finance for 10/23 to 10/30.

[vi] Research report from Epsilon Theory, “The King is Dead. Long Live the King” dated 11/5/20.

[vii] Research report from Epsilon Theory, “The King is Dead. Long Live the King” dated 11/5/20.

[viii] While small companies as measured by the Russell 2000 small-cap index has had six 10%+ multi-day moves in 2020, per Bespoke Investment Group, the number of underlying companies with negative profits appears to be quite large relative to history and could pose a problem if investors just buy the index versus those stocks which have positive earnings.

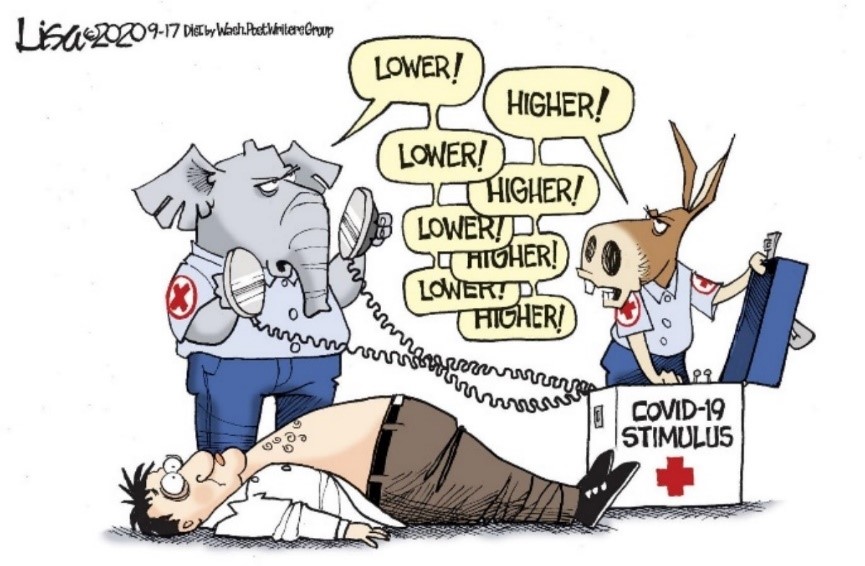

CIG Asset Management Update September 2020: Continuing Stimulus Hope

Summary:

- Stocks fell in September as big technology companies faltered [i] .

- COVID-19 deaths hit a grim milestone in the U.S. and increased around the world [v] .

- The markets traded up or down based upon the probability of a new stimulus bill.

Commentary:

The S&P 500 declined -3.9% and the tech-heavy NASDAQ dropped -5.2%.[i] Outside of the U.S., developed markets, as measured by the MSCI EAFE net, were down -2.9% and the MSCI Emerging Markets Index retreated -1.8%.[ii] Little protection was offered by Gold as it moved -4.1% lower as the US Dollar Index gained +1.9%.[iii] Fixed income (the Barclays U.S. Aggregate Total Return Index) returned -0.1% and the Barclays U.S. High Yield Index fell -1.0% for the month.[iv]

Republicans and Democrats struggled to come to an agreement to provide more stimulus to the economy. Republicans in the Senate were unable to pass their own “skinny” stimulus bill on September 10. Meanwhile, markets traded lower throughout the month as the COVID-19 death toll in the United States continued to increase and finally surpassed 200,000 on September 22.[v] Over the following two days, there were no less than sixteen Federal Reserve speeches in two days, but investors were unimpressed. Fed speakers reasserted that the Fed will do what it takes to support the economy and cautioned that what is really needed right now is more fiscal stimulus. On September 25, economy re-opening hopes blossomed when Governor DeSantis announced on that he was lifting all restrictions on the Florida economy. The following Monday, stimulus hopes were re-ignited as Speaker of the House Nancy Pelosi said she was hopeful to get a $2.4 trillion coronavirus stimulus bill passed.

September’s weakness in equities and their back and forth nature keep investors on notice that both the financial markets and the economy remain on thin ice. Uncertainty abounds and volatility could increase dramatically on short notice, especially as the election nears. Investors’ latest reminder was on October 6, when these stimulus machinations whipsawed the markets again.

We continue to employ diversification, discipline and flexibility in managing client portfolios to potentially avoid air pockets like the one above. Our focus on clients’ long term financial plans remains paramount.

Please join the team at CIG Capital Advisors for an engaging discussion looking at the challenges, opportunities and questions ahead as we navigate the current and future market conditions:

WEBINAR: “Keeping your Financial Plans Alive Amid Chaos”

Tuesday, October 20 at 6 p.m.

This report was prepared by CIG Asset Management and reflects the current opinion of the authors. It is based upon sources and data believed to be accurate and reliable. Opinions and forward-looking statements expressed are subject to change without notice. This information does not constitute a solicitation or an offer to buy or sell any security.

[i] Calculated from data obtained from Yahoo Finance, as of September 30, 2020

[ii] MSCI, as of September 30, 2020

[iii] Calculated from data obtained from Yahoo Finance, as of September 30, 2020

[iv] Calculated from data obtained from Bloomberg, as of September 30, 2020

[v] John Hopkins / NPR September 22, 2020

CIG Asset Management Update April 2020: Uncharted Territory

Equity markets embarked on their own version of the much hoped-for “v” shaped economic recovery during the month of April, even as economic data continued to record nasty numbers. The S&P 500(1) gained +12.7%, recovering much of the prior month’s losses. Outside of the U.S., the MSCI EAFE net(2) was up +6.5% and the MSCI Emerging Markets Index was up +9.2%(2). Within fixed income, the Barclays U.S. Aggregate Total Return Index (3) returned +1.8% and the Barclays U.S. High Yield Index(3) increased +4.5% for the month.

In April, there was a continued tug-of-war between economic reality and hopes that the worst of the pandemic may be behind us:

On Friday, April 3, it was reported that the March unemployment rate rose to 4.4%, the highest since August 2017.(4) Over the following weekend, many anecdotal news stories came out, spreading hope that COVID-19 was peaking. The ensuing Monday, April 8, the S&P 500 was up +7.03% for the day(5).

The weekly unemployment report on April 9 showed another 6.6 million in weekly claims(6), only to be quickly forgotten about as the Federal Reserve issued a statement within seconds of the Department of Labor release. The Fed announced a $2.3 trillion relief package including the Main Street Lending Program, to lend money to mid-sized businesses, and a municipal and corporate bond buying program. This latest Fed action put them far past anything they attempted during the 2008 Great Financial Crisis.

The April 16 weekly unemployment claims were 5.2 million(6), and the following day, a report that Remdesivir, an anti-viral drug may help treat symptoms of COVID-19, was made public.

Then on April 21, West Texas Intermediate oil futures settled at a negative number – never before had that happened! The following day, President Trump tweeted that we could shoot Iran boats down in the Persian Gulf, and of course, the oil and the stock markets rallied.

On April 23, weekly unemployment claims totaled 4.4 million(6). The following day, April 24, President Trump said that Apple CEO Tim Cook told him in a private conversation that he believes there will be a “v” shaped economic recovery, and markets moved higher.

April 30 weekly report brought another 3.8 million unemployed claims(6). The following weekend, several states began to gradually reopen their economies.

As can be clearly seen in the above timeline, every extremely negative economic statistic that was reported in April was met soon after by either a Federal Reserve announcement, a Trump tweet or positive news stories about pandemic hopes.

No rallies are more violent than bear market rallies and seeing April produce one of the most forceful rallies in decades fits that playbook. We would argue that the markets just followed a historic playbook given historic interventions on the monetary and fiscal fronts. Warren Buffett indicated at his May shareholders’ meeting that he’s not finding places of value to invest and has announced the selling of all airline shares with the view that the impacts of the recent crisis will not magically disappear but will take time to filter through the system.

In the meantime, what is driving the performance of the S&P 500 Index? To oversimplify, it comes down to five companies; Facebook (FB), Amazon (AMZN), Apple (AAPL), Microsoft (MSFT) and Alphabet (GOOGL). The acronym that most on Wall Street use is FAAMG. Year-to-date through April 30, the FAAMG stocks are up an average of +10% versus the other 495 companies in the S&P 500 down -13%(7).

The performance spread between the FAAMG stocks and rest of the S&P 500 will most likely narrow over time. The lagging 495 stocks could begin to catch up with the leaders, FAAMG could start underperforming, or a combination of the two.

We have mentioned before that it’s not possible to forecast the path of the pandemic. In contrast to the above, states reopening and the massive Federal stimulus have already produced “green shoots” suggesting that the economy could begin to recover. Starbucks announced on May 5 they planned to open 85% of its locations by the end of the week, with contactless pickup and cashless payments. Simon Properties, the country’s largest shopping mall operator, announced it would open malls as states allow it. Recent activity on the Apple map app is showing signs that driving activity is starting to rebound. We would especially like to strike an optimistic tone on that last point.

Here at CIG we continue to be proactive and nimble as we see how long this bear market rally and tug-of-war can continue.

This report was prepared by CIG Asset Management and reflects the current opinion of the authors. It is based upon sources and data believed to be accurate and reliable. Opinions and forward-looking statements expressed are subject to change without notice. This information does not constitute a solicitation or an offer to buy or sell any security.

SOURCES:

- Calculated from data obtained from Yahoo Finance, as of May 1, 2020.

- MSCI, as of May 1, 2020

- NEPC

- Bureau of Labor Statistics, April 3, 2020

- Calculated from data obtained from Yahoo Finance, as of May 1, 2020

- United States Department of Labor.

- FactSet, Goldman Sachs Global Investment Research

Financial Resiliency Amid Disruption: Your Healthcare Practice

Your medical or dental practice may have to adjust to a “new normal” as states slowly return to broader care permissions after weeks or months of tight, lockdown restrictions. Have you taken advantage of the programs offered to help medical and dental practices survive and what changes can you make to help ensure your practice thrives in a post-lockdown environment?.

Here are some management aspects dentists and physician-owners may want to consider in planning for financial resiliency amid the global disruption brought by the pandemic:

Cash Flow Summary

With so much uncertainty, being able to visualize your cash flows for the next 12 months is crucial. Taking proactive measures to forecast your incoming cash flows will allow you to implement a strategy early on and to timely take appropriate steps. The process includes analyzing your historical revenue stream and collection rates with an objective to forecast your future collections. Reviewing your procedure mix will help you determine what the impact of delaying non-essential procedures will be to your top-line.

Expenses should be adjusted to reflect cost management strategies and cash inflows from government establishments and banking institutions should be factored in to estimate cash balances throughout the pandemic as well as into the recovery period. Conducting a sensitivity analysis may also be beneficial to envision best case/worst case scenarios.

Telehealth

During the COVID-19 crisis, CMS has significantly expanded access to telehealth services for Medicare beneficiaries. This includes the easing of many of the stringent regulations set place by various government entities. Time should be spent reviewing the latest changes, highlighting the different opportunities available to you, and researching different telehealth platforms to see which is most appropriate for your practice.

Due diligence should also be conducted to highlight services that you may virtually perform and bill via telehealth. Disseminating the service to your patients as well as the general public is key to optimizing this tool.

A/R Management

Insurance companies don’t typically pay out as fast as many dental and medical practice managers would like. Understanding tools available to healthcare providers during the crisis could allow you to speed up your collection process. For example, CMS is expanding its payment acceleration program and HHS has announced a provider relief program. Your billing staff may also be utilized to effectuate collections through aggressive A/R management.

Expense Management

Having a handle on your expenses is one key to sustaining a positive cash flow. A first step may be to look into your historical expenses as a percentage of revenue as well as the year-over-year trends. Recent changes should be taken into consideration as well to prudently forecast your budget.

Fixed expenses are typically the biggest threat. However, there may be options available to you depending on the language in your contracts. Review the contracts and agreements you have in place and look for ways to renegotiate with an objective to defer or abate payments. It may be in your best interest to terminate some agreements.

Grant and Loan Opportunities

Keeping businesses up and running is almost just as crucial to owners as it is to the economy. For that reason, there are many grants and loans available to assist you with perfecting your payroll, rent and other costs. Time should be spent pinpointing your situation, reviewing various programs available to you, and working with your financial institution and accountant to pursue loan programs, grants, and line of credits to supplement your cash reserves.

Business Continuity and Recovery Planning

Having a Business Continuity Plan in place is imperative not only to weather crisis times but also to transition back to what many are calling the new normal. This involves reviewing your remote work capabilities, adjusting staff tasks to keep them engaged, increasing oversight of vendors, and other organizational modifications.

Let us help

As experienced medical and dental practice business advisors, we can dig deeper into your numbers and show where you can make changes that will improve your practice’s bottom line. Let us help support your practice’s resiliency by scheduling an initial complimentary consultation with Brian Lasher.